Cash vs. Accrual Accounting: Differences and Guidance (2026)

Cash vs. accrual accounting: key differences, IRS rules under IRC Section 448, Form 3115 guidance, and a decision framework for accounting professionals.

A practical guide to choosing between cash and accrual accounting, explaining how each method impacts financial reporting, tax obligations, and compliance. It outlines IRS requirements, key trade-offs, and when accrual becomes essential for growing, multi-entity, or investor-backed businesses.

In this article

The cash vs. accrual accounting decision affects how every transaction hits your books, how your tax liabilities are calculated, and whether your financial statements are acceptable to auditors, investors, and lenders.

This guide covers the mechanics of both methods, the IRS rules that remove the choice from many businesses, and a practical framework for accounting professionals advising clients on which method fits their accounting system.

Cash vs. Accrual Accounting: At a Glance

Cash accounting records revenue when cash is received and expenses are paid. Accrual accounting records revenue when it’s earned and expenses when they’re incurred, regardless of when cash moves.

For most accounting professionals, accrual is the default: it’s required by GAAP, generally required by the IRS above certain revenue thresholds (subject to §448 exceptions), and is the only method that produces GAAP-compliant consolidated financials across multiple entities.

Cash Accounting

Accrual Accounting

Revenue recognized when

Cash is received

Revenue is earned (invoice issued/service delivered)

Expenses recognized when

Cash is paid out

Expense is incurred (bill received/liability created)

Accounts receivable tracked

❌

✅

Accounts payable tracked

❌

✅

GAAP compliant

❌

✅

IFRS compliant

❌

✅

IRS availability

Only below the inflation-adjusted §448(c) threshold (~$30M in recent years, with exceptions)

Always permitted

Best for

Micro businesses, sole proprietors, simple cash flows

Cash basis accounting is a method where transactions are recorded only when cash changes hands.

Revenue is booked when a customer pays; an expense is booked when the business pays a bill. There’s no need to track receivables, payables, or accruals.

❓ Cash accounting is the simpler of the two methods. The books reflect what’s in the bank at any given moment, making it straightforward to understand and maintain without a dedicated accounting team.

Here’s how it works in practice:

Scenario

When Cash Records It

Client is invoiced in December, pays in January

January (when cash arrives)

Supplies ordered in November, paid in December

December (when payment leaves)

Annual insurance premium paid upfront in January

January (full amount, no amortization)

Contractor completes work in March, invoice paid in April

April (when cash is paid)

What Are the Advantages of Cash Basis Accounting?

Cash accounting works well when simplicity and cash visibility are the priority. Here’s what makes working with it a breeze:

Simple to maintain: You don’t need to track receivables, payables, or accruals; the bank statement is essentially the ledger.

Clear cash flow visibility: The books show exactly what cash is available right now.

Tax deferral potential: Income isn’t taxable until received, which can help smaller businesses manage tax timing.

Lower administrative overhead: No complex adjusting entries, no deferred revenue schedules, and no prepaid expense amortization.

What Are the Disadvantages of Cash Accounting?

The same simplicity that makes cash accounting easy to maintain also limits what it can tell you.

Distorted financial picture: A business can show a profitable month simply because large invoices were collected, even if those invoices relate to prior periods.

Not GAAP or IFRS compliant: Financial statements prepared on a cash basis can’t be audited under OCBOA frameworks but aren’t acceptable for GAAP and IFRS reporting. This disqualifies a business from most institutional investment and public financing.

IRS restrictions apply: Most businesses above the inflation-adjusted §448(c) gross receipts threshold (approximately $30M in recent years) are required by the IRS to use accrual; C corporations face the same restriction.

Can’t support multi-entity consolidation: Consolidated financials require matching revenues and expenses across entities in the same period; cash accounting can’t do this reliably.

No matching principle: Expenses and the revenues they generate may fall in different periods, producing misleading profitability reports.

What Is Accrual Basis Accounting?

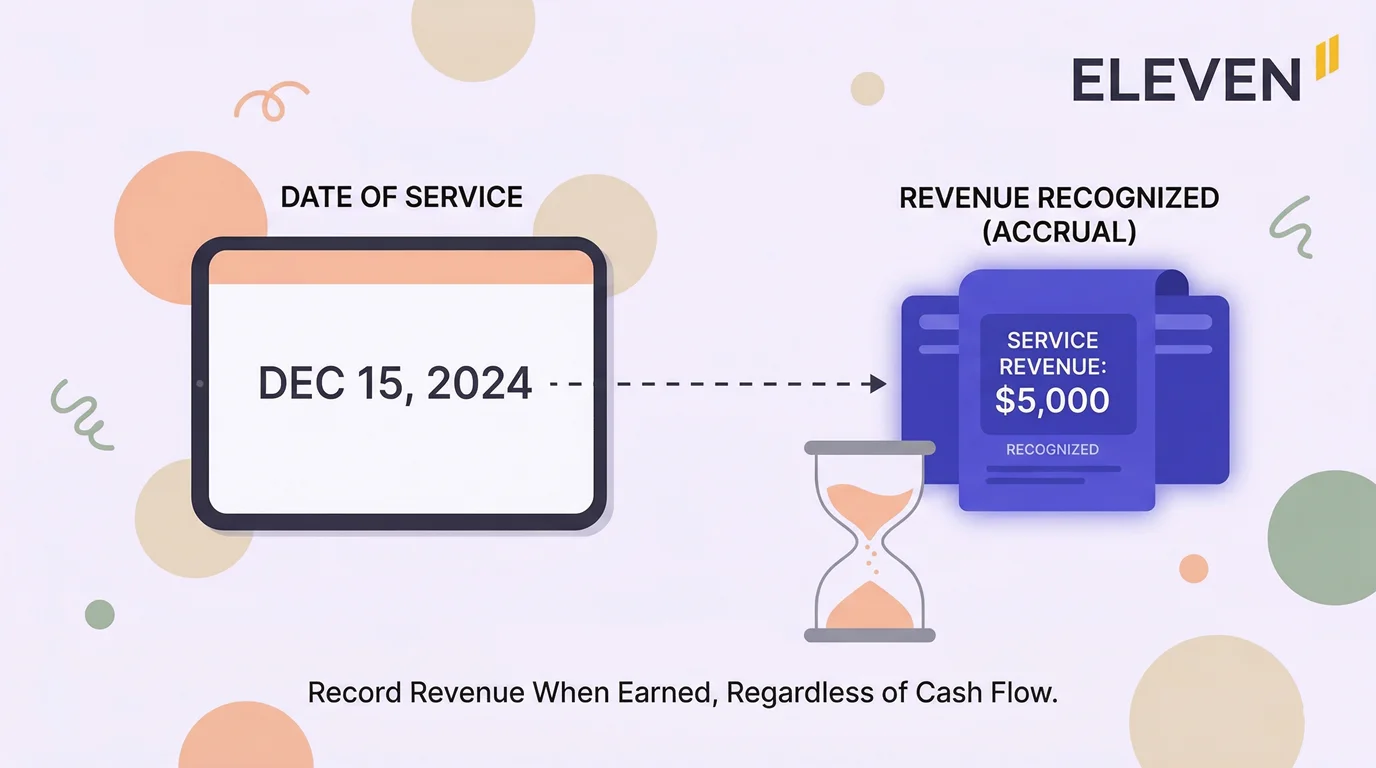

Accrual basis accounting records revenue when it’s earned and expenses when they’re incurred, regardless of when cash changes hands. A delivered invoice is revenue even before the client pays; a received bill is an expense even before the check is written.

This method produces financial statements that reflect the economic reality of the period, not just the cash activity.

❓ The accrual method is the foundation of GAAP and IFRS. It’s required for all publicly traded companies, generally required by the IRS for most businesses above the §448(c) gross receipts threshold (subject to statutory exceptions including farming businesses and qualified personal service corporations), and is the only method that produces meaningful consolidated financials across multiple entities or currencies.

Here’s how it works in practice:

Scenario

When Accrual Records It

Client is invoiced in December, pays in January

December (when service was delivered)

Supplies received in November, paid in December

November (when obligation was created)

Annual insurance premium paid upfront in January

Monthly (amortized across 12 periods)

Contractor completes work in March, invoice paid in April

March (when work was performed)

What Are the Advantages of Accrual Accounting?

Accrual accounting’s strength is that it reflects economic reality, not just cash movement.

Accurate financial picture: Revenues and expenses are matched to the periods they belong to, producing financial statements that reflect actual performance.

GAAP and IFRS compliant: It’s auditable, acceptable to investors and lenders, and required for public company reporting.

Supports multi-entity and consolidated reporting: Entities can produce meaningful group financials because revenue and expense timing is consistent across all books.

Better for forecasting and budgeting: Management can see what’s owed and what’s due without waiting for cash to move.

Required above IRS revenue thresholds: Compliance is built in; there’s no risk of a forced mid-year method change if the business grows.

What Are the Disadvantages of Accrual Accounting?

Accrual accounting’s accuracy comes with trade-offs, particularly in complexity and cash flow visibility.

Does not show cash position directly: A business can be highly profitable on paper while running low on actual cash; it requires a separate cash flow statement to manage liquidity.

More complex to maintain: It requires tracking receivables, payables, prepaid expenses, deferred revenue, and accrued liabilities; meaning it needs competent accounting software or personnel.

Adjusting entries required at period-end: Accruals, deferrals, and prepayments need to be reviewed and adjusted each period to keep the books accurate.

Potential to overstate revenue: Revenue is recognized before cash arrives; if clients don’t pay, bad debt expense must be recorded after the fact.

Cash vs. Accrual Accounting: Side-by-Side Comparison

Here’s how the two methods compare.

Cash Accounting

Accrual Accounting

Records when cash moves

Records when cash is earned or incurred

No receivables or payables

Full AR/AP tracking

Simple, low overhead

More complex but more accurate

Good for cash flow visibility

Shows true financial performance

Tax deferral possible

Tax paid on earned income

Not GAAP/IFRS compliant

GAAP and IFRS compliant

Limited to smaller businesses (IRS rules)

Required above IRS revenue thresholds

Can’t support consolidated reporting

Supports multi-entity consolidation

When Does the IRS Require Accrual Accounting?

The IRS requires accrual accounting in several situations. It mandates accrual accounting for the following:

C corporations and partnerships with C corporations above the inflation-adjusted §448(c) gross receipts threshold (approximately $30M based on a 3-year average).

Tax shelters regardless of size.

Farming businesses and qualified personal service corporations are exempt from the restriction.

✅ Note that post-TCJA, businesses below the §448(c) threshold can use cash accounting even with inventory under §471(c), treating inventory as non-incidental materials and supplies. The IRS accrual requirement is conditional, not absolute, meaning statutory exceptions apply.

The Tax Cuts and Jobs Act (2017) introduced a simplified accounting method election under IRC Section 448, which expanded access to cash-basis accounting for smaller businesses.

Here’s how the current rules break down:

Entity Type

Cash Accounting Allowed?

Threshold/Condition

Sole proprietors and single-member LLCs

✅

Generally permitted; not subject to §448(a) directly, but §446 "clearly reflect income" standard applies at scale. Consult a tax professional if gross receipts are growing significantly.

Partnerships (no C corporation partners)

✅

3-year avg. gross receipts below the §448(c) inflation-adjusted threshold (~$30M in recent years).

S corporations

✅

Generally permitted without a revenue threshold; S corps are not subject to §448(a)(1) directly. Restricted only if the entity is a tax shelter or falls into specific edge cases.

C corporations

⚠️ (Limited)

Below the §448(c) inflation-adjusted threshold (~$30M in recent years) AND not a tax shelter

C corporations (farming)

✅

Special farming exception applies

Businesses with inventory

⚠️ (Restricted)

Businesses below the §448(c) threshold can use cash under §471(c), treating inventory as non-incidental materials and supplies; above the threshold, accrual is generally required for inventory.

Tax shelters

❌

Accrual required regardless of size or entity type

Publicly traded companies

❌

GAAP (accrual) required by SEC for all public filings

⚠️ The §448(c) threshold is inflation-adjusted, not fixed at $30M, and is a 3-year average. The base amount under IRC §448(c) is $25,000,000, adjusted annually for inflation since 2018. In practice, this has ranged from approximately $26M to $31M depending on the year. The test uses the average the prior three tax years. A single year above the threshold doesn’t disqualify a business; only when the 3-year average exceeds the threshold does the restriction apply in the following tax year.

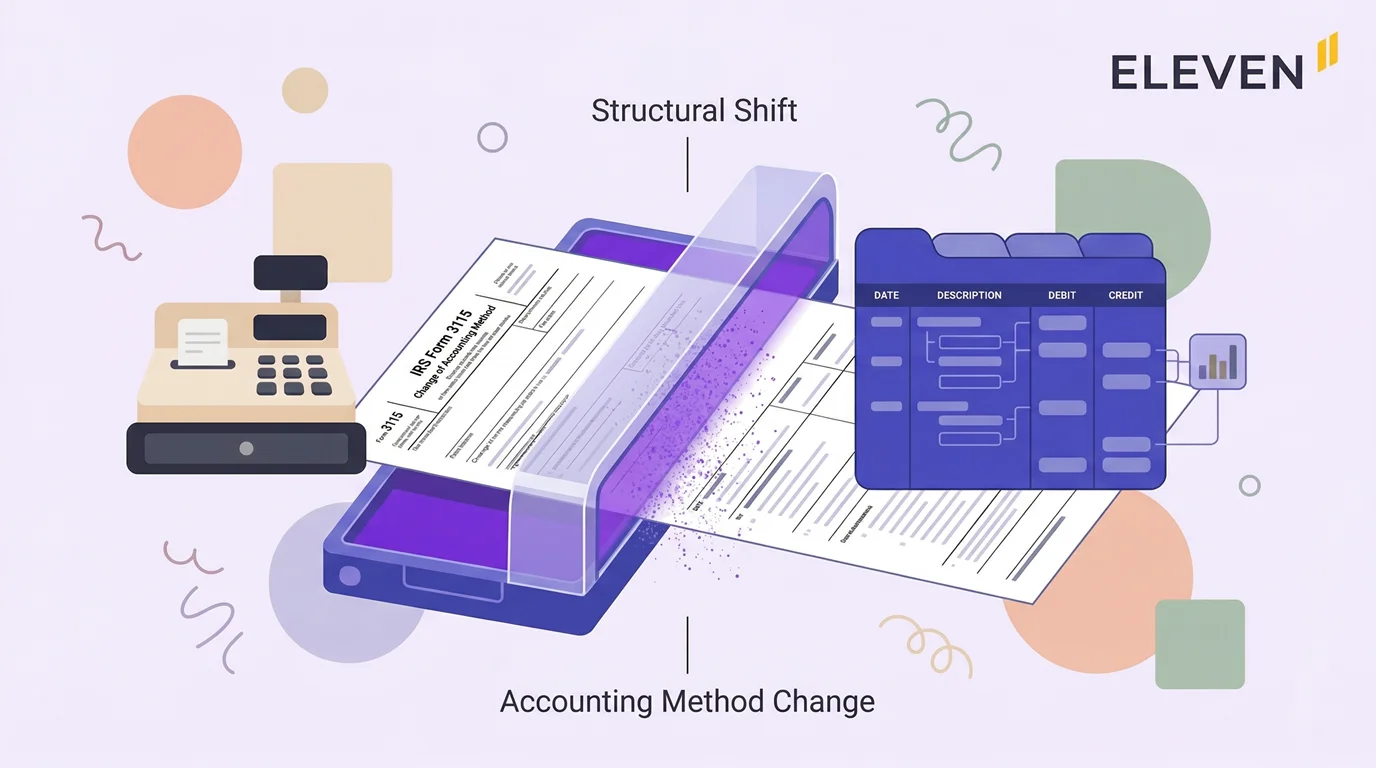

A method change from cash to accrual requires filing Form 3115 (Application for Change in Accounting Method) with the IRS. This isn’t optional and carries specific timing requirements.

❓ Farming businesses, qualified personal service corporations, and entities that aren’t tax shelters may qualify for exceptions to the restriction even above the threshold. These statutory exceptions matter in practice and should be evaluated before assuming accrual is required.

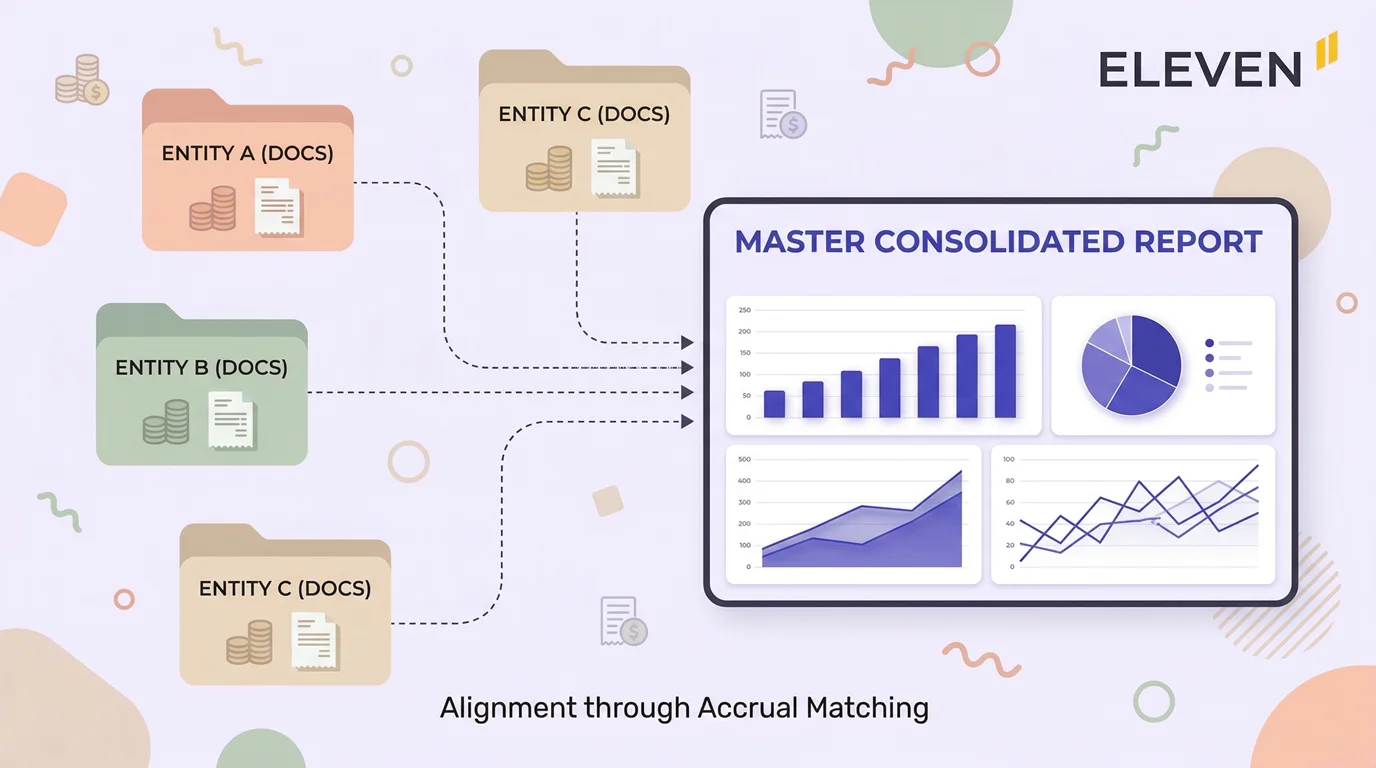

Cash vs. Accrual Accounting for Multi-Entity Firms

Accrual accounting is the only practical method for producing GAAP-compliant consolidated financial statements across multiple entities.

While cash-basis consolidation is theoretically possible via manual adjustments, it’s not GAAP-compliant and not operationally viable at professional scale. Cash accounting can’t reliably match intercompany revenues and expenses across entities in the same period, which makes group reporting unreliable.

❓ Any CPA firm or family office managing multiple client entities should operate on accrual across all entities.

This is where the cash vs. accrual debate becomes a non-debate for your practice. Consider what consolidated reporting requires:

Revenue recognition consistency: If Entity A uses accrual and Entity B uses cash, an intercompany service transaction may be recognized in different periods across the two books, creating artificial timing differences in the consolidated statement.

Elimination of intercompany transactions: Intercompany eliminations require matching the revenue on one entity's books to the expense on another's; cash accounting can’t guarantee they land in the same period.

Currency translation for multi-currency entities:IAS 21 and ASC 830 both require accrual-based financial statements as the starting point for foreign currency translation; cash-basis books can’t be IFRS or GAAP translated.

Investor and lender reporting: Any consolidated financial statement presented to an external party will be expected to comply with GAAP or IFRS; both require accrual.

If your firm produces consolidated financials for a client group, all entities in the group need to use the same accounting method and the same period-end dates. A client group where one subsidiary uses cash and another uses accrual creates a consolidation problem that can’t be solved cleanly at the reporting layer.

→ When onboarding a new client group, confirm the accounting method and period-end consistency before the first close.

Cash vs. Accrual Accounting: How to Choose

Start with the IRS rules if you’re unsure whether to use cash or accrual accounting.

If the business exceeds the inflation-adjusted §448(c) gross receipts threshold (approximately $30M in recent years based on a 3-year average), carries significant inventory, or is a C corporation above the threshold, accrual is required, unless a statutory exception applies.

Below those thresholds, the decision comes down to business complexity, growth trajectory, and reporting requirements. Here’s a breakdown of the conditions:

Here’s a decision matrix based on your current situation; use it to find out whether you should be using cash or accrual accounting:

Use Cash Accounting If…

Use Accrual Accounting If…

The business is a sole proprietor, freelancer, or single-member LLC with simple, predictable cash flows

The IRS requires it based on entity type, revenue threshold, or inventory rules

Annual gross receipts are well below the §448(c) inflation-adjusted threshold with no near-term growth plans that would push past it

The business carries inventory, runs significant accounts receivable, or has deferred revenue

There is no inventory, no significant credit sales, and no need to produce GAAP-compliant financial statements

Financial statements will be presented to investors, lenders, or auditors

Tax deferral of receivables has a meaningful cash benefit and the business wants to manage taxable income timing

The business is growing and is likely to cross the §448(c) inflation-adjusted threshold within the next two to three years

The client is a small service business with no external investors or institutional lenders requiring audited financials

The client is part of a multi-entity group that requires consolidated reporting

—

The business has international operations requiring IFRS or ASC 830-compliant currency translation

—

The firm is advising on valuation, M&A, or capital raises where GAAP financials are a requirement

Switching from Cash to Accrual: What to Know

Switching from cash to accrual requires filing Form 3115 (Application for Change in Accounting Method) with the IRS. The change produces a Section 481(a) adjustment, which accounts for the cumulative income and expense differences between the two methods.

This adjustment is typically spread over four years to avoid a large one-time tax impact. However, a method change isn’t a simple settings toggle. Here’s what the process involves:

File Form 3115: The application must be filed with the IRS and, in most cases, attached to the tax return for the year of change; automatic consent procedures apply for most voluntary changes.

Calculate the Section 481(a) adjustment: This represents the difference in income and expenses that would have been recognized under the new method; positive adjustments (additional income) are spread over four years, negative adjustments may be taken in the year of change.

Restate opening balances: Receivables, payables, prepaid expenses, deferred revenue, and accrued liabilities all need to be recorded for the first time as opening balances.

Update accounting software configuration: The chart of accounts needs to reflect accrual-basis accounts; existing transactions may need reclassification.

Communicate to stakeholders: If financial statements are shared with investors or lenders, disclose the method change and provide comparative data where possible.

⚠️ Plan the change before the threshold, not after. The most common error is waiting until a business crosses the IRS threshold before beginning the method change process. Form 3115 takes time to prepare correctly, and the Section 481(a) adjustment can be significant for a business that has been on cash basis for several years.

If a client is on a growth trajectory that will push them past the §448(c) inflation-adjusted threshold within the next one to two years, begin the transition early. A voluntary method change made before the threshold is crossed gives more flexibility on timing and adjustment treatment.

How Accounting Software Handles Cash vs. Accrual

Most cloud accounting platforms support both methods, but depending on your firm's complexity, the depth of accrual support varies significantly.

Basic platforms like QuickBooks and Xero allow you to toggle between cash and accrual views for reporting, but they’re not purpose-built for the multi-entity accrual workflows that CPA firms require.

Platforms like Eleven are built around accrual from the ground up, with multi-entity general ledgers, automated period-end accruals, and consolidated reporting across entities and currencies as core functionality.

What to Look for in Accounting Software for Accrual-Based Firms

Here's what to look for when evaluating accounting software for your firm.

Multi-entity general ledger: Each entity should have its own chart of accounts and accrual-basis books, with cross-entity navigation and consolidated reporting built in.

Automated bank reconciliation: AI-powered matching should handle the volume that accrual-basis multi-client firms generate; manual reconciliation doesn’t scale.

Period-end accrual management: The platform should support deferred revenue recognition schedules, prepaid expense amortization, and accrued liability tracking without manual journal entries for each.

Consolidated reporting across entities: Group financials should generate natively from the platform; exporting to Excel for consolidation is a sign the software architecture doesn’t match the workload.

Multi-currency with IAS 21 revaluation: For firms with international clients, the platform needs to handle FX revaluation at period-end, not just currency conversion on transactions.

Audit trail and document management: Accrual-basis financials produce more complex supporting documentation; the platform should store and link source documents to every entry.

Eleven and Accrual Accounting

Eleven is built for accrual-basis accounting at scale. Every entity operates on its own accrual-basis general ledger, with automated bank reconciliation, AI-powered invoice extraction, and native consolidated reporting across all entities in a chosen reporting currency.

For CPA firms managing multi-entity client groups, the architecture matches the actual workflow: accrual by default, consolidation built in, and period-end close supported without spreadsheets.

What is the main difference between cash and accrual accounting?

Cash accounting records transactions when cash moves. Accrual accounting records them when they’re economically earned or incurred. For example, a December invoice paid in January is December revenue under accrual but January revenue under cash.

Over time, accrual produces financial statements that reflect actual business performance; cash accounting reflects cash movement.

Which is better: cash or accrual accounting?

Accrual accounting is more accurate and is the standard required by GAAP, IFRS, and the IRS above certain thresholds. Cash accounting is simpler and can be appropriate for very small businesses with straightforward cash flows and no external reporting requirements.

For most businesses working with professional accounting firms, accrual is the right method.

Can a small business use cash basis accounting?

Yes, if it meets the IRS criteria. Sole proprietors, single-member LLCs, S corporations, and partnerships without C corporation partners can use cash accounting if the 3-year average of annual gross receipts is below the inflation-adjusted §448(c) threshold (approximately $30M in recent years).

Businesses that carry significant inventory face additional restrictions. The simplicity benefit is real for very small operations, but any business on a growth path toward institutional investment or public financing should plan to move to accrual early.

Is accrual accounting required by GAAP?

Yes. Generally Accepted Accounting Principles require accrual accounting for all financial statements prepared in compliance with GAAP. Cash-basis financial statements are not GAAP-compliant. They can be audited under Other Comprehensive Basis of Accounting (OCBOA) frameworks, but an OCBOA audit isn’t the same as a GAAP audit and isn’t acceptable for institutional financing, SEC reporting, or public markets.

Any business seeking GAAP-compliant audit opinions or public market listing must use accrual accounting.

What is the Section 481(a) adjustment when switching accounting methods?

When a business changes from cash to accrual accounting, it files Form 3115 with the IRS. The Section 481(a) adjustment accounts for the cumulative income and expense differences between the two methods up to the date of change.

A positive adjustment (additional taxable income) is generally spread over four tax years to smooth the impact. A negative adjustment (a deduction) can typically be taken in full in the year of change.

Can you use cash accounting for some transactions and accrual for others?

Generally no, but there are limited exceptions. The IRS allows certain businesses to use the cash method for some activities and the accrual method for others, but these hybrid approaches are narrowly defined and require careful compliance.

For most businesses and their accounting firms, using a single consistent method across all transactions is the practical and compliant approach.

How does the choice of accounting method affect multi-entity consolidated reporting?

It affects it significantly. Consolidated financial statements require consistent revenue and expense recognition timing across all entities in the group. If entities in a group use different methods, intercompany eliminations become unreliable and the consolidated income statement will contain timing distortions.

Accrual accounting is required for any client group producing consolidated financials for external stakeholders.

Saad Mouaouine is an SEO content writer, editor, and AI-focused researcher specializing in long-form digital content, automation-assisted workflows, and search optimization. He has written and edited hundreds of articles across technology, SaaS, and business-focused industries, contributing to projects connected to global brands including Shell plc. At Eleven, he helps create SEO-driven content focused on accounting technology, automation, and operational efficiency.

.avif)