Types of Accounting Systems: Choosing the Right Architecture

Not all accounting systems are built the same. Learn how flat ledgers, dimensional systems, and multi-entity platforms differ and which scales with your firm.

Most accounting discussions stop at features and price. This guide goes deeper, covering ledger architecture, multi-entity consolidation, multi-currency compliance, and AI readiness, so CPA firms and family offices can choose a system that actually scales with their practice.

In this article

Most accounting systems were designed for one company, one currency, and one accountant. That's fine, until it isn't.

For CPA firms managing dozens of client entities and family offices overseeing complex, internationally distributed assets, the standard types of accounting systems taxonomy don’t map to the decisions you're actually making.

The relevant questions are structural: how the ledger handles scale, how the system manages consolidation across entities, and whether multi-currency is a core accounting function or a display feature. That's where this guide starts.

What Are the Main Types of Accounting Systems?

There are four main ways to classify accounting systems: by recording method, revenue timing, delivery model, and ledger architecture. Each determines something different about how the system handles your data and scales with your firm.

Before we get into architecture, it's worth dispensing with the basics. Not because they're unimportant, but because they set up the more meaningful distinctions that follow.

Scalability, reporting depth, and consolidation capability

The first three rows are familiar territory. The fourth (ledger architecture) is where most accounting professionals should be focusing their attention and where most software comparisons fall completely short.

📌 Key Insight:Double-entry bookkeeping and accrual accounting aren’t differentiators in 2026; they’re baseline requirements. Any professional-grade system takes them as given. The meaningful question is how the ledger underneath is structured.

What Is the Difference Between a Flat Ledger and a Dimensional Ledger?

A flat ledger tracks variables by creating new account codes for each combination of department, project, or entity.

A dimensional ledger attaches those variables as metadata tags on individual journal lines instead. The result is a smaller, cleaner chart of accounts that can be filtered and analyzed across any combination of dimensions without structural changes.

This is the architectural distinction that most accounting software comparisons never reach, and it’s the one that determines whether your system can grow with your firm or eventually collapse under its own complexity.

The Flat Ledger Problem: Chart of Accounts Bloat

Traditional accounting software is built around a segmented chart of accounts. Every variable you want to track (a department, a geography, a cost center, or a project) requires a new account code.

→ On paper, this sounds manageable. In practice, it creates what controllers privately call chart of accounts bloat.

Here’s a simple example of how quickly this compounds:

Variable

Options

Account Codes Generated

Revenue Type

3 (services, products, and advisory)

3

+Region

4 (US, EU, APAC, LATAM)

12

+Department

5 (tax, audit, advisory, FP&A, ops)

60

+Entity

10 clients

600

+Year

3 years of history

1,800

1,800 account codes to track what is, fundamentally, one revenue concept across a few dimensions. Now multiply this across your full chart of accounts. The result is a ledger that becomes increasingly difficult to navigate, prone to coding errors, and nearly impossible to query flexibly.

⚠️ Real-World Consequence: Chart of accounts bloat is one of the leading causes of delayed month-end closes. When accountants spend time hunting through hundreds of similar account codes or correcting miscoded entries, that time compounds across every client, every month, every year.

The Dimensional Ledger: Metadata Over Multiplication

Dimensional accounting solves this by separating the core economic concept from the attributes used to analyze it.

→ Instead of creating new account codes for every variable, dimensions are applied as metadata tags on individual journal lines.

Here’s what it looks like compared to the flat ledger approach. The same scenario as above, restructured:

Element

Flat Ledger Approach

Dimensional Approach

Base Accounts

1,800 codes

~60 core codes

New Region Added

+600 account codes

Add 1 dimension value

New Client Added

+180 account codes

Add 1 entity

Reporting Flexibility

Fixed (structure baked in)

Ad hoc (filter any combination)

Coding Error Risk

High (similar codes)

Low (structured selection)

With a dimensional ledger, a single account (e.g., 4,000 in revenue) can be filtered and analyzed by region, department, entity, or project without any structural change to the chart of accounts.

The ledger stays clean, the analysis stays flexible, and when you add a new client or open a new office, you add a dimension value, not two hundred account codes.

💡 Pro Tip: When evaluating accounting software, ask this specific question: “If I add a new operating entity, how many changes does my chart of accounts require?” A flat-ledger system will give you a large sum. A dimensional system should give you zero.

What Makes a Multi-Entity Accounting System Different?

Single-entity accounting is a solved problem. The tools are mature, the workflows are standardized, and the choices are mostly about price and interface.

Multi-entity accounting is an entirely different discipline, and most software wasn’t built for it.

The Consolidation Challenge

When a firm manages multiple entities (whether that's ten client companies, a family office with a dozen subsidiaries, or a holding structure with regional operating businesses), the accounting challenge shifts from record-keeping to consolidation.

Consolidation requires:

Intercompany elimination: removing revenue and expense recorded on both sides of a transaction between related entities so the group financials don't double-count.

Due-to/due-from tracking: managing intercompany balances that must net to zero at the group level.

Non-controlling interest (NCI): when a parent owns more than 50% but not 100% of a subsidiary, the minority share must be isolated and correctly presented on the consolidated balance sheet under ASC 810/IFRS 10.

Currency translation: restating each subsidiary's financials into the presentation currency before consolidation.

In a system not built for this, every single one of these steps is a manual export to a spreadsheet. The process looks like this:

Step

Without Multi-Entity System

With Native Multi-Entity System

Extract subsidiary data

Export each entity separately

Unified database (no export needed)

Intercompany elimination

Manual journal in Excel

Automated (system identifies and eliminates)

NCI calculation

Spreadsheet formula

Calculated natively from ownership structure

Consolidated trial balance

Re-keyed into master file

Available in real time, on demand

Audit trail

Fragmented across files

Single, immutable record across all entities

📊 Industry Data:74% of family offices still rely on general-purpose systems and spreadsheets for general ledger accounting. The manual consolidation risk this creates (version control errors, incorrect eliminations, and delayed closes) is significant and largely invisible until an audit.

The Per-Entity Pricing Trap

There’s a commercial dimension to multi-entity accounting that doesn’t get discussed enough: how your software charges for it.

Many cloud accounting platforms use per-entity pricing. Every time a CPA firm onboards a new client (or a family office establishes a new subsidiary), the software bill increases. Growth is literally penalized.

→ The alternative is per-accountant (or per-user) pricing, where the number of entities is unlimited. For a CPA firm managing 50 or 200 clients, this changes the unit economics of the entire practice. The software cost becomes predictable, tied to headcount rather than client growth.

💡 Pro Tip: When evaluating accounting software, ask your vendor: “What happens to my subscription cost when I add a new entity?” If the answer involves a per-entity fee, model out the cost at your firm’s target scale before signing anything.

How Does Multi-Currency Support Work in Accounting Systems?

Multi-currency is one of those features that every accounting platform claims to support and almost none handle correctly at the infrastructure level.

There’s a meaningful difference between a system that converts invoice display values into a secondary currency and one that manages currency at the ledger level throughout the entire accounting lifecycle.

Functional Currency vs. Presentation Currency

Professional multi-currency accounting starts with a distinction that most software glosses over entirely:

Concept

Definition

Why It Matters

Functional Currency

The currency of the primary economic environment in which an entity operates

Each entity in a group may have a different functional currency

The group may present in USD even if subsidiaries operate in EUR, SGD, or JPY

A system that only supports one base currency per account forces firms to choose between recording transactions in the entity’s functional currency or the group’s presentation currency. This is a compromise that creates errors in both directions.

FX Revaluations and IAS 21 Compliance

Under IAS 21 (The Effects of Changes in Foreign Exchange Rates), monetary items (cash, receivables, and payables) must be retranslated at the closing rate at each balance sheet date. The resulting foreign exchange gains and losses must be recognized in profit or loss.

This means at every period-end, a properly built system should:

Retrieve the closing exchange rates for all monetary items in nonfunctional currencies

Calculate the difference between the historical rate (when the transaction was recorded) and the closing rate.

Post the resulting realized and unrealized FX variance to the correct P&L account automatically

Generate the disclosures required under IAS 21, including the net FX impact for the period

When this process is manual (as it often is with generic accounting software), it introduces the risk of period-end errors that compound across entities and currencies. A family office managing investment structures in the US, Europe, and Singapore can’t afford to run FX revaluations through a spreadsheet.

📌 2025 Regulatory Note: The IASB issued amendments to IAS 21 in 2023, effective for annual periods beginning on or after January 1, 2025. These amendments address “lack of exchangeability”: situations where a currency can’t be converted to another due to legal restrictions or market conditions. Entities must now estimate spot rates using a prescribed methodology and provide enhanced disclosures. A modern accounting system should handle this natively.

What Role Does AI Play in Modern Accounting Systems?

AI in accounting refers to the use of machine learning and automation to handle tasks that were previously manual: reading invoices, matching bank transactions, categorizing expenses, and generating reports.

What started as basic data capture has evolved into autonomous workflows capable of executing multi-step processes without human input at every stage.

Here’s how AI can help with accounting tasks.

Data Capture and Autonomous Workflows

The first wave of AI in accounting was about data capture: OCR-driven invoice extraction, automated bank feed matching, and basic transaction categorization.

These capabilities reduced manual data entry, but they still required a human to review and approve every output.

The profession is now moving into a more consequential phase. Industry data shows that AI adoption in accounting firms jumped from 9% in 2024 to 41% in 2025 because the technology crossed a reliability threshold that made it trustworthy enough for production use.

Here’s a quick breakdown:

Generation

Capability

Human Role

Current Status

Gen 1: OCR / Extraction

Read and parse invoice data from PDFs and images

Reviews every output

Fully commoditized

Gen 2: Automation (Copilot)

Suggests matches, flags anomalies, and routes approvals

Approves suggestions

Industry standard (2024–2025)

Gen 3: Agentic AI

Executes multi-step workflows autonomously within defined governance rules

Sets rules and reviews exceptions

Emerging (2025–2026)

Data Quality Prerequisites

This is the part most AI in accounting conversations skip entirely: autonomous agents are only as good as the data structure underneath them.

An agentic system capable of processing invoices in 10 seconds, matching 90–95% of bank transactions automatically, and running nightly variance analyses requires a clean, structured ledger to operate against.

If the chart of accounts is bloated, if intercompany transactions are inconsistently coded, or if entities are managed in separate files rather than a unified environment, the AI's accuracy collapses.

⚠️ The Automation Readiness Test: Before evaluating AI capabilities in any accounting platform, ask this: “Is my underlying data structured well enough for automation to be reliable?”84% of finance teams still spend at least 25% of their time on manual, repetitive work despite existing software investments. The bottleneck is usually not the AI; it’s the ledger architecture it runs on top of.

What Agentic AI Looks Like in Practice

For CPA firms and family offices operating at scale, agentic accounting infrastructure means the following:

Invoices uploaded (digitally or as scans) are processed and coded in seconds, with AI accuracy around 96%, flagging only exceptions for human review.

Bank reconciliation runs automatically across all entities, with the system identifying matched transactions and queuing only unmatched items for accountant attention.

Period-end close tasks (journal entries, accruals, and FX revaluations) are generated based on rules defined by the accounting team, not executed from scratch each month.

Reporting is generated on demand, with consolidated financials available in real time rather than assembled the day before a board meeting.

How Is AI Changing the Role of the Accountant?

When AI handle data entry, bank matching, and period-end close tasks, the accountant's time frees up for work that requires judgment: analysis, client advisory, and strategic planning.

Clean books have always been the baseline expectation. What clients and stakeholders increasingly want from their accounting professionals is interpretation (what the numbers mean, what's coming, and what to do about it). AI creates the conditions for that shift by removing the volume work that previously consumed most of the available capacity.

For firms that embrace this, the service offering changes meaningfully:

Instead of spending the first two weeks of each month closing books, the team spends that time reviewing dashboards, flagging anomalies, and advising clients on cash flow, tax exposure, or entity structure.

The accountant becomes a strategist with access to real-time data, not a processor catching up on last month's entries.

→ The firms that fall behind won't be the ones that adopted AI too late. They'll be the ones whose data architecture wasn't structured well enough for AI to run reliably on top of it.

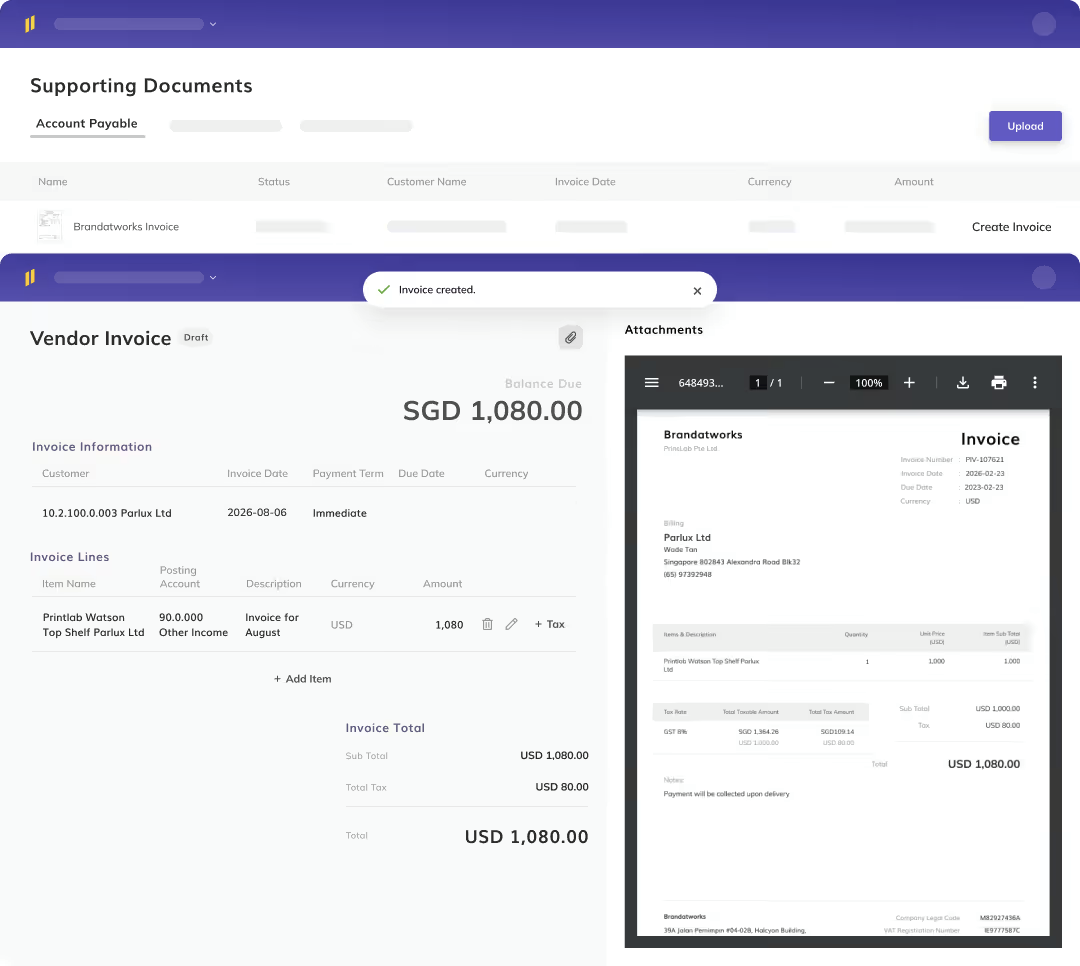

Why Does Integrated Document Management Matter in Accounting Systems?

This is a feature category that doesn't get the attention it deserves in software comparisons, possibly because it sounds administrative. It isn't.

Audit readiness is the clearest lens through which to evaluate document management. When an auditor requests supporting documentation for a transaction, the question is simple: How long does it take to retrieve it?

In a system where financial data and documents live in separate places (accounting software in one platform and invoices and contracts in a shared drive or email), that retrieval process involves multiple systems, multiple logins, and a meaningful risk of version control errors or missing files.

In a system with native document management, every invoice, receipt, contract, and statement is stored in the same environment as the transaction it supports. The document is attached directly to the journal entry. An auditor (or an accountant) can pull the full supporting file in one click.

Here’s a quick comparison:

Scenario

Without Integrated DMS

With Integrated DMS

Auditor requests invoice for transaction

Search email, shared drive, ask client

One click from the journal entry

Client queries an expense entry

Cross-reference multiple systems

Document is attached and is visible immediately

Month-end close documentation

Assemble manually from folders

Automatically linked as entries are posted

Version control for amended contracts

Risk of using outdated file

Full version history in one place

📌 Security Standard: Professional document storage in an accounting context should include role-based access controls (so client documents are only visible to authorized staff), AES-256 encryption at rest, and an immutable audit log of every document access event. These are the baseline for handling client financial data.

Which Type of Accounting System is Right for CPA Firms and Family Offices

The answer depends on the complexity of what you’re managing. Below is a direct framework.

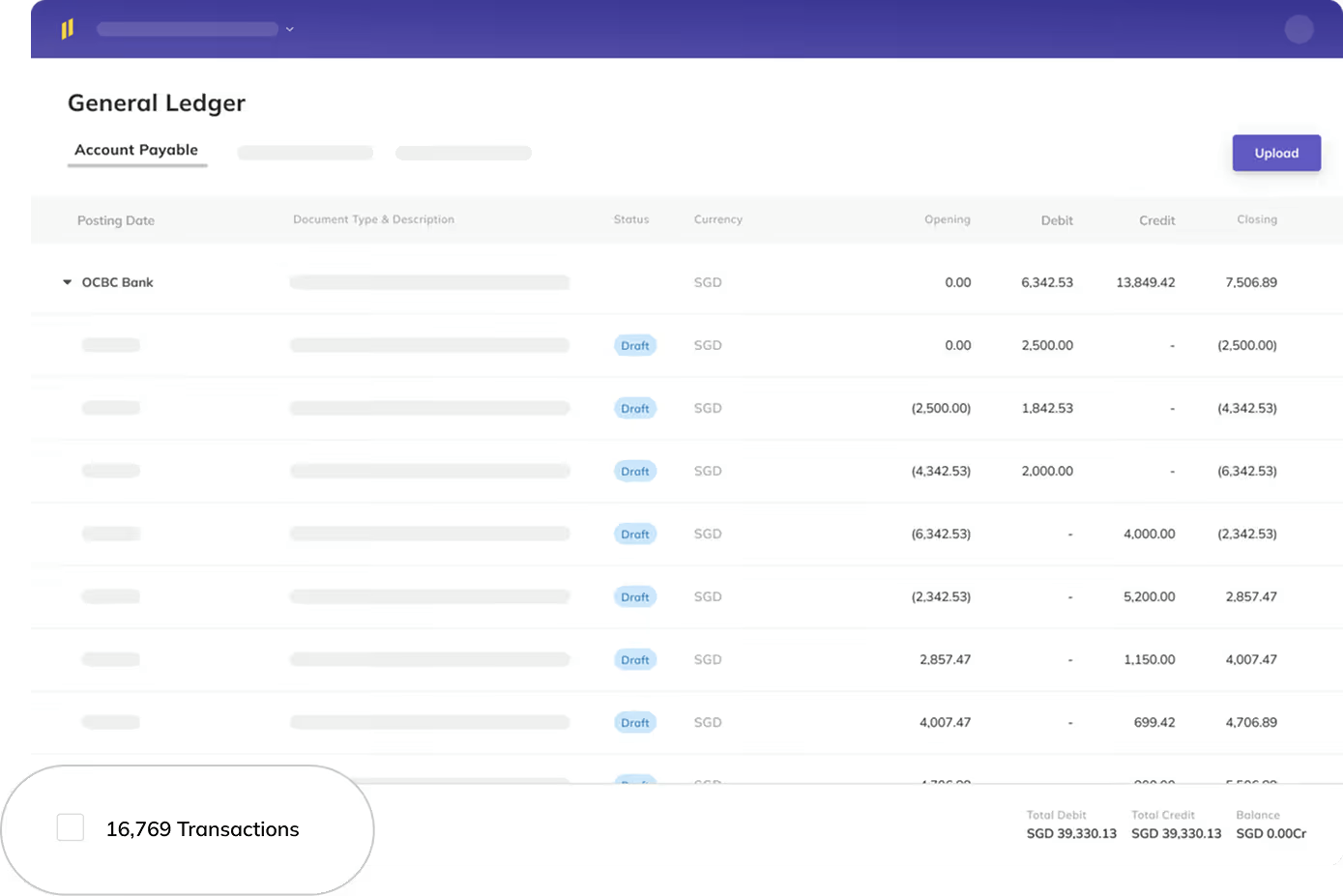

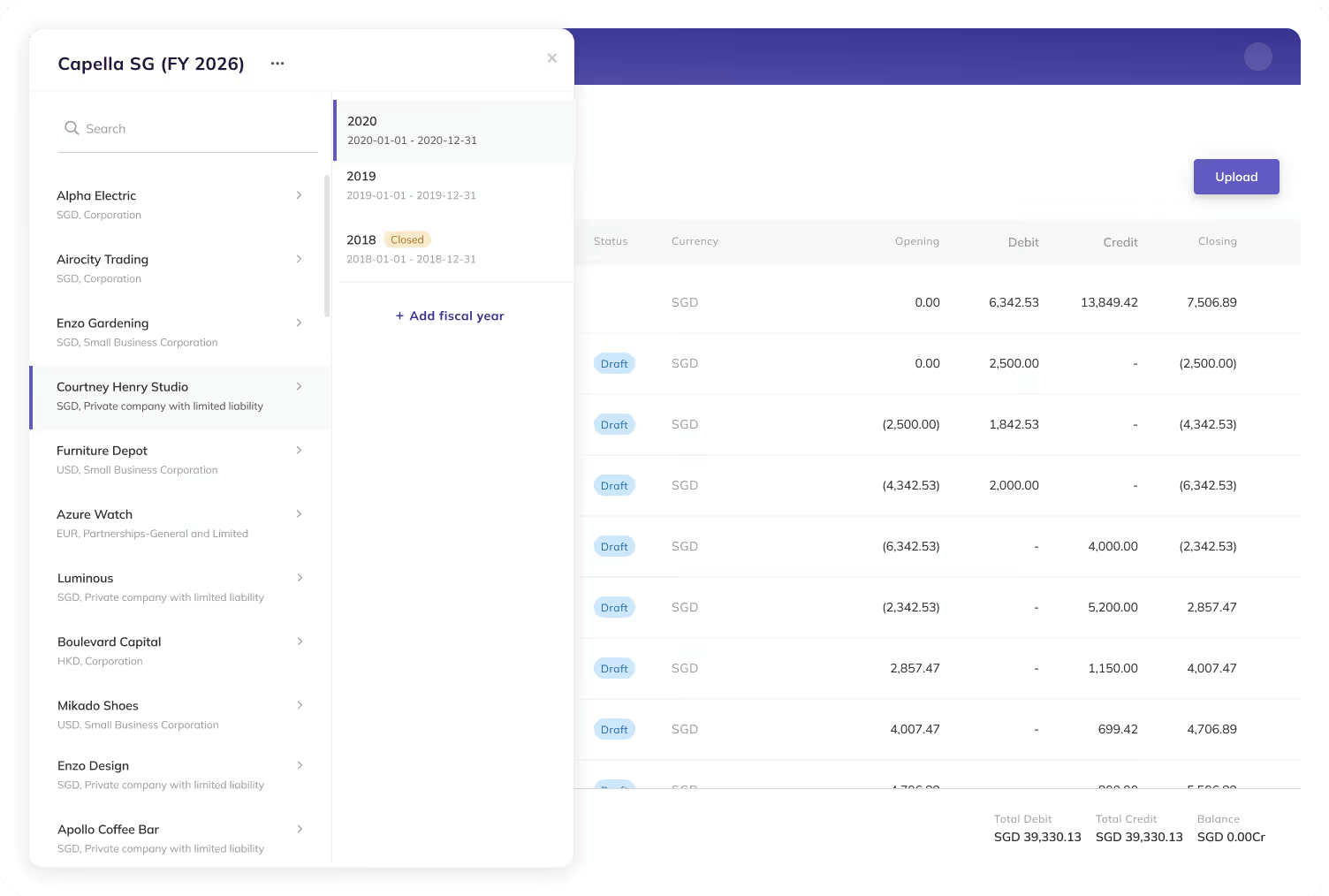

Eleven is an AI-powered accounting platform designed specifically for CPA firms and family offices managing multi-entity, multi-currency environments.

It’s built around the architecture described in this guide: a scalable general ledger, native multi-company management, automated bank reconciliation, AI-driven data extraction, and an integrated document management system through Dokmee.

A few specifics worth noting for professionals evaluating infrastructure:

Entity model: Each client or company operates in its own database within a unified platform. There’s no file-switching; accountants move between entities from a single dashboard.

Currency support: 170+ currencies, with automatic exchange rate updates, realized and unrealized FX gain/loss calculations, and IAS 21-aligned revaluations.

AI accuracy: Invoice processing with ~96% data extraction accuracy, reducing manual entry to exception-handling only.

Bank reconciliation: Automated matching across all connected accounts, with 90–95% of transactions matched without manual intervention.

Pricing: Per-accountant, not per-entity. Client growth does not increase your software costs.

Your Architecture Decision Is Your Strategy Decision

Most firms approach accounting software as a feature comparison: who has the better bank feed, the cleaner interface, or the lower monthly price? That’s the wrong frame.

The choice of accounting architecture determines the ceiling of how complex an engagement you can handle, how fast you can close, how confidently you can consolidate, and how much your firm can grow without adding proportional headcount.

The accounting profession is in the middle of a structural shift. AI adoption at firms jumped from 9% to 41% in a single year. The firms that will benefit most are not the ones who adopted AI last; they’re the ones who built their data architecture well enough that AI has something solid to run on top of.

That starts with the ledger. And it starts now.

Frequently Asked Questions (FAQs)

What is the difference between a flat ledger and a dimensional ledger?

A flat ledger tracks variables by creating new account codes for each combination of department, entity, or project, leading to chart of accounts bloat as complexity grows.

A dimensional ledger attaches metadata tags (dimensions) to journal lines, allowing a single core account to be filtered and analyzed across any combination of attributes without expanding the chart of accounts.

What accounting system is best for a CPA firm managing multiple clients?

A native multi-entity platform with per-user (not per-entity) pricing, consolidated reporting, and AI-driven automation.

The key requirements are the ability to manage unlimited client entities from a single dashboard, produce consolidated financials without spreadsheet exports, and automate routine tasks like bank reconciliation and invoice processing.

How does multi-currency accounting work in professional systems?

Professional multi-currency accounting manages currency at the ledger level, assigning a functional currency to each entity and a presentation currency for consolidated reporting.

At period-end, monetary items are retranslated at closing rates and the resulting foreign exchange variances (realized and unrealized) are posted automatically, in compliance with IAS 21.

What is agentic AI in accounting?

Agentic AI refers to systems that execute multi-step accounting workflows autonomously (processing invoices, matching bank transactions, and generating accruals) within defined governance rules, rather than just suggesting actions for a human to approve.

It’s the next generation beyond “copilot” AI, which still requires human approval of each suggestion.

Why does integrated document management matter for accounting software?

When documents (invoices, contracts, and receipts) live in a separate system from the accounting ledger, retrieving supporting evidence during an audit or client query requires navigating multiple platforms with the risk of version control errors.

Integrated document management links each file directly to its corresponding transaction, making documentation retrieval instant and audit trails complete.

What is the difference between cash basis and accrual accounting?

Cash basis records revenue when cash is received and expenses when cash is paid. Accrual accounting records revenue when earned and expenses when incurred, regardless of cash movement.

Accrual basis is required under GAAP and IFRS for most professional engagements and provides a more accurate picture of financial performance over time.

Can accounting software handle non-controlling interest calculations automatically?

Purpose-built multi-entity platforms can calculate non-controlling interest (NCI) as part of the consolidation process, based on the ownership percentages defined for each subsidiary.

This eliminates the need for manual NCI calculations in Excel (a common source of consolidation errors) and ensures compliance with ASC 810 and IFRS 10.

Saad Mouaouine is an SEO content writer, editor, and AI-focused researcher specializing in long-form digital content, automation-assisted workflows, and search optimization. He has written and edited hundreds of articles across technology, SaaS, and business-focused industries, contributing to projects connected to global brands including Shell plc. At Eleven, he helps create SEO-driven content focused on accounting technology, automation, and operational efficiency.

.avif)