7 Best Cloud-Based Accounting Solutions for Accounting Firms and CPA Practices (2026)

Last updated:

March 18, 2026 5:24 AM

8

min read

Written by

Noel Bouwmeester

Reviewed by

Noe Saglio

Accounts Receivable Fraud: What It Is, How It Happens, and How to Prevent It

Most AR fraud doesn't start with a scandal. It hides inside routine invoicing, write-offs, and payment posting. This guide breaks down how it happens, what to watch for, and how to stop it early.

Accounts receivable fraud doesn't announce itself. It compounds quietly through skimmed payments, manipulated write-offs, and fake invoices that look routine until they don't. This guide walks through the most common schemes, the warning signs that surface before losses grow, and the process controls that make fraud significantly harder to pull off.

In this article

Every year, organizations lose an estimated 5% of their annual revenue to fraud.

Not through elaborate schemes, but through routine accounting activity. Accounts receivable is one of the most common places it hides: frequent transactions, direct ties to cash, and processes that often run on trust more than controls.

What makes it difficult to catch is how unremarkable it looks.

Over 40% of fraud cases are uncovered through tips, not audits, meaning most of it runs quietly until someone says something.

This article covers how it happens, why it persists, and what actually reduces the risk.

What Is Accounts Receivable Fraud?

Accounts receivable fraud is any intentional manipulation of receivables-related transactions for personal or organizational gain. That includes altered invoices, intercepted payments, unauthorized credits, and fabricated write-offs.

What makes it dangerous is how normal it looks.

Receivables balances may still appear reasonable. Cash flow may seem healthy. Revenue may look on track. But if someone has been interfering with your billing or collections process, the financial picture you're relying on isn't real.

Most AR fraud falls under asset misappropriation, the most common category of occupational fraud globally, though it can also cross into financial statement fraud when fake receivables are used to inflate revenue. In either case, the longer it runs undetected, the wider the gap between what your books show and what's actually there.

What Is Receivables Fraud?

You may see receivables fraud and accounts receivable fraud used interchangeably, and in most cases that is fine. But receivables fraud is technically broader. It covers any fraudulent activity involving money your business is owed, including cases where nothing is directly stolen.

That means internal misconduct like stolen payments or unauthorized write-offs, but also external behavior like intentional nonpayment or altered remittance details, and subtler situations where your receivables are simply being misstated or delayed.

What all of these have in common is the damage they do to your financial visibility. The gap between what your books show and what you actually collect grows quietly, and the longer it goes unaddressed, the harder it becomes to get an accurate read on your own business.

An Example of Accounting Fraud Involving Receivables

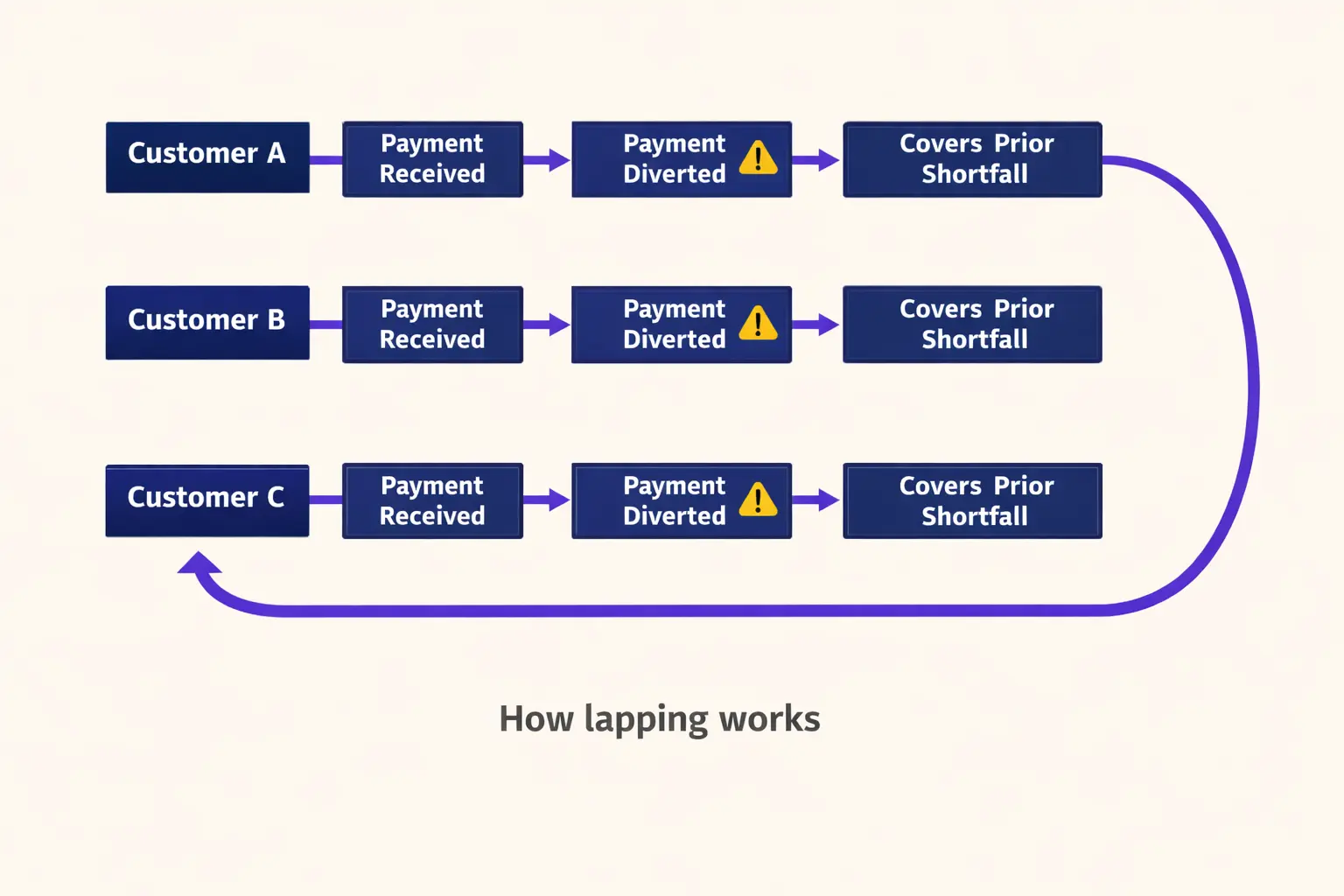

One of the most common receivables fraud schemes is lapping, and it has a way of hiding in plain sight.

Here is how it typically works: an employee receives a payment from Customer A, pockets it, and never records it. When Customer B's payment arrives, it gets applied to Customer A's account to cover the gap. Customer C's payment covers Customer B. The cycle continues, each new payment masking the last theft, until something disrupts it.

That disruption is often the only thing that stops it.

Consider the case of Jennifer Renee Bivens, a former clerk at the Fulton Electric System in Kentucky. An audit identified more than $81,000 in missing funds and revealed that Bivens had been taking money from her cash drawer and using checks from a later date to cover the shortage. She was convicted of theft by a Fulton Circuit Court jury in 2011.

The scheme worked because Bivens controlled the cash drawer and the records. Lapping relies on one person handling cash receipt, payment posting, and reconciliation without oversight.

When those duties are concentrated in a single employee, the cycle can run quietly for months. The accounts appear to reconcile. Timing differences explain away the gaps. No single transaction looks suspicious on its own.

Other Common Types of Accounts Receivable Fraud

Most accounts receivable fraud follows a small number of repeatable patterns. The schemes themselves are not particularly sophisticated. What makes them effective is how well they blend into normal accounting activity.

- Skimming: An employee intercepts a payment before it is ever recorded. No accounting entry is created, so there is nothing to reconcile and no trail to follow unless a customer disputes a balance or an external confirmation surfaces the gap.

- Fictitious sales and fake customers: Invoices are created for transactions that never happened, inflating both revenue and receivables simultaneously. This scheme is often linked to performance pressure or bonus targets, and it can run undetected for a long time because the numbers look like growth.

- Unauthorized write-offs and credits: A valid receivable gets written off without approval, or a credit is issued and the difference quietly diverted. These adjustments frequently get buried in miscellaneous line items, where they attract little scrutiny.

- Manipulated journal entries: Unsupported or late manual entries override controls, mask shortages, and smooth over discrepancies. They tend to cluster near period-end or audit deadlines, exactly when they are least likely to be questioned.

What connects all of these is not complexity. It is opportunity. Each scheme persists where oversight is thin and no one is looking closely enough to ask why the numbers look the way they do.

Is Accounts Receivable Fraud Really That Common?

Yes, and it is probably more common in your organization than you think. Global occupational fraud research shows that asset misappropriation appears in nearly 90% of all fraud cases, making it the most common category worldwide.

Accounts receivable is especially exposed. The function involves frequent, high-value transactions tied directly to cash, and fraud has a natural cover story: receivables increase, sales look strong, collections lag slightly. In a growing business, those patterns look completely normal.

The risk compounds when a single employee controls multiple steps in the receivables lifecycle. Posting payments, applying credits, reconciling balances.

When one person owns all of that, there is no second set of eyes to catch what is going wrong. Fraud can continue for a long time without triggering any alarms, even when the rest of your accounting looks perfectly fine.

What Are the Top 3 Types of Fraud?

Most people think of fraud as one clear-cut thing. If you manage receivables, the reality is messier than that. Organizational fraud generally falls into three categories, and your AR process touches all of them.

- Asset misappropriation: stealing or misusing company resources. Most AR fraud starts here.

- Corruption: bribery, kickbacks, and conflicts of interest. In a receivables context, that can mean unauthorized discounts, improper write-offs, or someone on your team quietly benefiting from how payments are handled.

- Financial statement fraud: making your numbers look better than they are, often through fake invoices or inflated receivables.

The reason this matters is the overlap. A small theft in your collections process can turn into a reconciliation problem, then a reporting problem. Each step makes it harder to find and harder to fix.

Red Flags That Signal Accounts Receivable Fraud

Accounts receivable fraud rarely starts with a single obvious event. It reveals itself through patterns across financial data, operations, and behavior.

🚩 Financial red flags

- Accounts receivable growing faster than revenue

- Aging balances increasing without a clear business reason

- Frequent or unexplained manual adjustments

- Mismatches between bank deposits and recorded receipts

🚩 Operational red flags

- High volume of write-offs or credits

- Excessive customer discounts

- Activity in dormant or rarely used customer accounts

- Repeated corrections to payment applications

🚩 Behavioral red flags

- Employees refusing to take time off

- Resistance to sharing duties or documentation

- Unusual control over specific processes or reports

🚩 Customer-driven red flags

- Customers claiming invoices were paid but still appear open

- Disputes over invoice amounts or payment timing

- Requests for duplicate invoices more frequently than normal

Note: No single red flag confirms fraud. Consistent patterns do. A one-off manual adjustment or a delayed deposit can have innocent explanations. But when the same signals keep surfacing, around the same person, the same accounts, or the same time of month, that pattern deserves attention. Most fraud persists not because it is invisible, but because the signs get rationalized away one at a time.

Why Accounts Receivable Fraud Happens

Most accounts receivable fraud does not happen because someone set out to steal. It happens because three things align at the same time: pressure, opportunity, and a way to justify it.

The pressure can come from anywhere. Personal debt, job insecurity, an aggressive bonus target, or a culture that rewards revenue growth at any cost. Employees facing that kind of strain do not always look for the most obvious way out.

Sometimes they look at the cash flowing through their hands every day and see a temporary solution.

Opportunity is what turns that pressure into action.

Weak controls, limited segregation of duties (the practice of dividing financial tasks across multiple people so no single employee controls an entire process), and processes built on trust rather than oversight create openings that are easy to exploit.

Receivables functions in particular tend to evolve informally, especially in small or growing teams, leaving gaps that nobody has formally addressed because nothing has gone wrong yet.

Rationalization is what keeps it going. Very few people think of themselves as criminals. They tell themselves it is temporary, that they will pay it back, that the company can afford it, that they deserve it after years of being underpaid.

Those justifications are remarkably durable, and they are what allows a small theft to quietly compound into a material loss over months or years.

Understanding this matters because it shifts the question. The goal is not to identify which of your employees might crack under pressure. It is to design processes where opportunity is limited enough that pressure and rationalization never get the chance to become action.

What Happens If Fraud Goes Unchecked?

The real cost of unchecked AR fraud is not just what gets stolen. It is everything that breaks down around it.

Losses accumulate quietly, often for years. Meanwhile your financial statements are telling a story that is not true. Receivables look healthier than they are, revenue appears stronger than it is, and every decision made on that data carries hidden risk.

Customer trust erodes in parallel. Disputed invoices and unexplained balances create friction that damages relationships before anyone connects it to fraud. In regulated environments, that friction can escalate into compliance failures, penalties, and legal consequences that far outlast the original scheme.

And then there is reputation. Financial losses can be quantified and recovered. The confidence of clients, auditors, and regulators, once lost, is much harder to earn back. That is often the damage that lingers longest.

How to Detect Accounts Receivable Fraud Earlier

The challenge with detecting AR fraud early is that the signs are easy to explain away individually. Catching it requires consistency, not just occasional scrutiny.

- Reconcile bank deposits to receivables frequently. Gaps between what was received and what was recorded are where fraud hides. The longer those gaps go unexamined, the harder they are to unwind.

- Explain timing differences, don't assume them. A deposit that shows up a few days late has an innocent explanation until it doesn't. Make it a habit to ask why, not just note that it happened.

- Review aging reports for patterns, not just totals. A receivables balance can look healthy in aggregate while individual accounts are quietly deteriorating. Look at what is moving and what is not.

- Scrutinize manual journal entries, especially near period close. Unsupported entries that appear at month-end or before an audit are one of the most consistent signals of fraud across all scheme types.

- Use customer confirmations as an external checkpoint. Customers know what they paid. Periodic statements and confirmations introduce a perspective that internal records alone cannot provide, and they remain one of the most effective detection tools available.

Above all, no single person should control invoicing, cash application, and reconciliation. When one person owns all three, the usual checks simply do not exist. That is not a technology problem or a staffing problem. It is a process design problem, and it is the single most important thing you can fix.

How to Prevent Accounts Receivable Fraud

Preventing AR fraud is less about catching bad actors and more about designing processes that do not give fraud room to grow.

The most effective place to start is segregation of duties.

When invoicing, cash application, and reconciliation are handled by different people, no single employee has the access needed to commit and conceal fraud on their own. This one change eliminates a significant portion of your exposure.

Beyond that, approval policies matter.

Write-offs, credits, and adjustments should require sign-off, and that sign-off should come from someone who did not originate the transaction. Without a defined threshold and a second set of eyes, these are some of the easiest places for fraud to hide.

Regular audits and independent reviews introduce the kind of scrutiny that daily operations rarely provide. They do not need to be exhaustive to be effective. The knowledge that records will be reviewed changes behavior on its own.

Technology supports all of this, but only if it is configured to do so. Audit trails, role-based access, and structured approval workflows reduce reliance on trust and make it significantly harder to manipulate records without leaving a trace.

Your people matter too. Employees who know what fraud looks like are more likely to notice when something feels off and more likely to say something. A confidential reporting channel gives them a way to do that without putting themselves at risk.

None of this requires suspicion. It requires processes that hold up under scrutiny, whether or not anything is actually wrong.

Final Thoughts: How Eleven Helps You Stay Ahead of AR Fraud

Accounts receivable fraud rarely starts as a crisis. It develops quietly, taking advantage of small gaps in your processes and oversight, and compounds until something forces it into the open.

Understanding how it works, recognizing the warning signs early, and putting the right controls in place significantly reduces your exposure. The more complexity you manage, whether across multiple clients, entities, or jurisdictions, the more that visibility matters.

Eleven is built specifically for this environment. If you run a CPA firm or manage a family office, Eleven gives you the multi-entity structure, document traceability, and workflow controls that make fraud significantly harder to pull off and much easier to catch early.

Automated workflows reduce the manual touchpoints where fraud tends to hide. Audit trails and linked source documents make every transaction traceable across every entity you manage. And role-based access means the right people see the right things, without relying on informal agreements or trust alone.

Software cannot prevent fraud on its own. But the right platform means your controls are easier to maintain, your records are harder to manipulate, and issues surface before they become material problems. Start a free trial of Eleven and see how it works in practice.

Guides

✔

Noel Bouwmeester

Noel Bouwmeester is an SEO content strategist and B2B SaaS writer focused on organic growth, search visibility, and AI-era content discovery. He has contributed to SEO and content marketing initiatives for companies including lempire and lemlist, helping support large-scale organic traffic growth through search-focused content strategies. At Eleven, he contributes educational SEO content focused on accounting technology, automation, and AI-driven business workflows.

.avif)