What is Bank Reconciliation?

What is bank reconciliation? Learn the essentials with Runeleven’s glossary guide—discover steps, benefits, and tips for accurate financial records.

Bank reconciliation is the process of comparing and matching the transactions recorded in your business’s cash book (or accounting records) with the transactions shown on your bank statement.

The goal is to make sure both records agree, that is, that your books accurately reflect the money that’s actually in your bank account.

By doing this, you can keep your financial data correct and current, spot discrepancies early, and help protect against fraud.

Companies do this on a regular basis to ensure their internal records match their bank statements. When any inconsistencies are found, they can be reviewed and resolved to keep financial statements accurate and trustworthy.

What is a bank reconciliation statement?

A bank reconciliation statement is a financial document that explains the differences between the balance shown in a company’s cash book and the balance shown on its bank statement at a particular date.

It is prepared after comparing both records to identify any discrepancies, such as outstanding cheques, deposits in transit, or unrecorded bank charges.

The purpose of a bank reconciliation statement is to ensure that the company’s accounting records accurately reflect the true amount of cash available in its bank account. It helps detect errors, omissions, or fraudulent transactions, and confirms that all financial information is up to date and reliable.

How to do bank reconciliation

Here’s a step-by-step process, to make bank reconciliation just 5 easy steps for you to follow:

- Get both records:

- Your bank statement (from the bank)

- Your cash book or accounting ledger (or accounting software)

- Compare transactions:

- Tick off all items that appear in both records (e.g., deposits, withdrawals, bank fees)

- Identify differences, such as:

- Outstanding cheques: written but not yet cleared by the bank

- Deposits in transit: money received but not yet reflected in the bank statement

- Bank charges or interest: may appear on the bank statement but not yet recorded in your books

- Errors: wrong amounts, duplicates, or omissions

- Adjust your cash book for any missing or incorrect entries.

- Prepare a reconciliation statement by calculating the adjusted balance.

- Start with the balance as per the bank statement

- Add any deposits in transit

- Subtract outstanding cheques

- Add or subtract any errors or adjustments until the adjusted balance matches your books

Why is bank reconciliation important?

Bank reconciliation is essential in order to keep accurate financial records and for the overall financial health of your business.

Without it, errors and discrepancies can go unnoticed, leading to badly managed finances, compliance issues, and negative impacts on performance and customer experience.

Benefits of bank reconciliation include early detection of errors, like duplicate transactions, incorrect entries, or missing deposits, and fraud prevention, by catching unauthorized withdrawals and forged checks sooner rather than later.

It will also improve your cash-flow management, by helping you avoid overestimating how much cash you actually have available, and giving you a clearer view of your financial position so you can make better-informed business decisions.

From a compliance perspective, bank reconciliation helps you meet tax obligations and regulatory requirements, avoiding audit issues and penalties.

It also helps prevent overdrafts by ensuring sufficient funds are available before issuing payments, protecting relationships with vendors and suppliers.

The most significant impact is on cash collection, where reconciliation directly affects revenue and customer experience.

When payments aren't applied correctly, it causes delays in cash inflow, redundant follow-ups, and frustrated customers - you might end up chasing customers who've already paid, or failing to follow up when money is owed.

How can Eleven help you with your bank reconciliations?

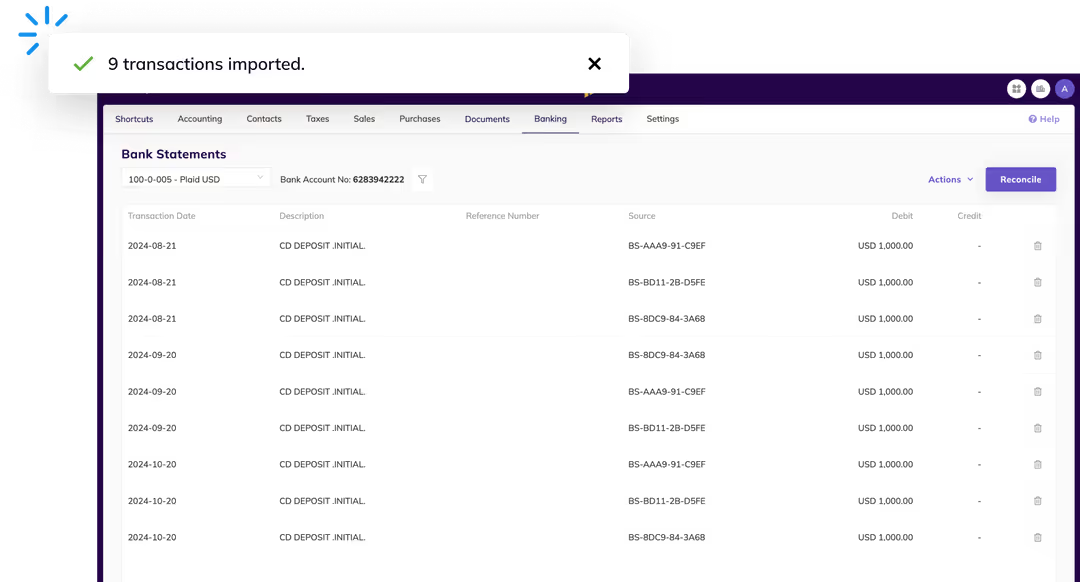

Eleven provides an automated bank reconciliation system that connects directly to your bank accounts and imports your financial transactions daily. Because the bank feed is live or frequently updated, your accounting software stays in sync with your bank, giving you a reliable, up-to-date picture of cash-flow.

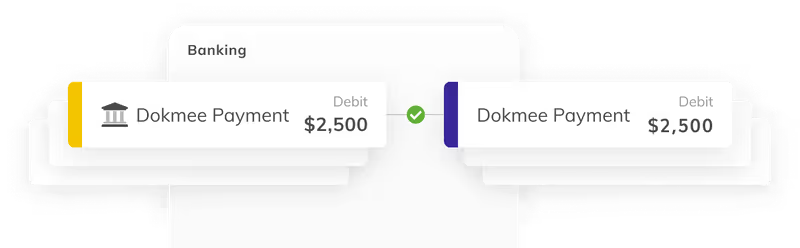

Once transactions are imported, Eleven makes reconciliation much easier by matching entries automatically. It finds the corresponding income or expense entries in your books and suggests matches, with just one click.

For transactions that don’t have an obvious match, the software flags them so you can review manually. This reduces the tedious work of comparing bank statements manually line by line and lowers the chance of missing something.

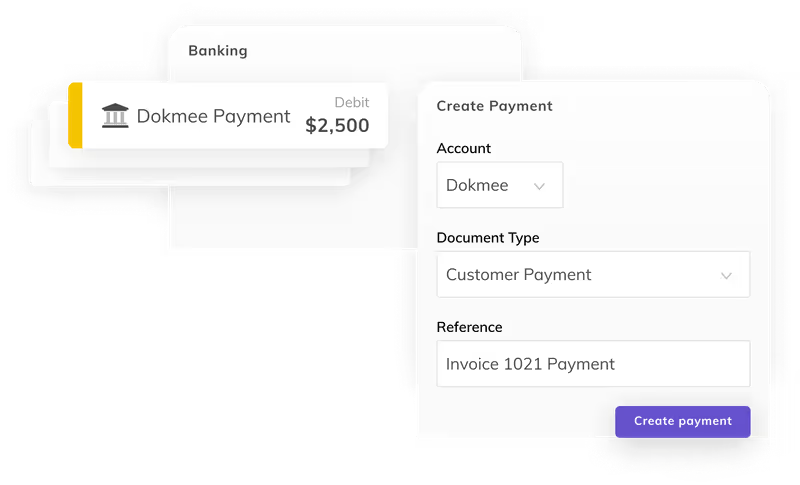

Moreover, Eleven lets you create payments and receipts from the imported bank transactions themselves, which helps in reconciling them immediately. If something appears on the bank side but not yet in your books (or vice versa), you can record it right there rather than waiting to discover it later.

Because the system is more automated, there’s less manual cross-checking, and discrepancies are caught earlier, not months later. It can also help you avoid common problems within bank reconciliation management like duplicate entries, omissions or missing entries, and timing differences, which could be confusing and costly for your clients or business.