What Is an Annual Report - And How Do You Actually Write One?

Guide to Annual Reports: Definition and Writing Tips

After the end of the financial year, the next important step is preparing the annual report. What's an annual report? This is information about the company's past, present, and future.

In this article

Every year, the same deadline sneaks up on firms and family offices alike: the annual report. And every year, the same questions arise: what goes in it, what format it needs to follow, and who is responsible for filing it.

The pressure is real, especially when your clients are counting on accuracy and your reputation depends on it.

This guide cuts through the noise. Whether you're preparing reports for a private equity firm, a family office, or a closely-held business, here's everything you need to know about annual reports: what they are, what they contain, and how to file them correctly.

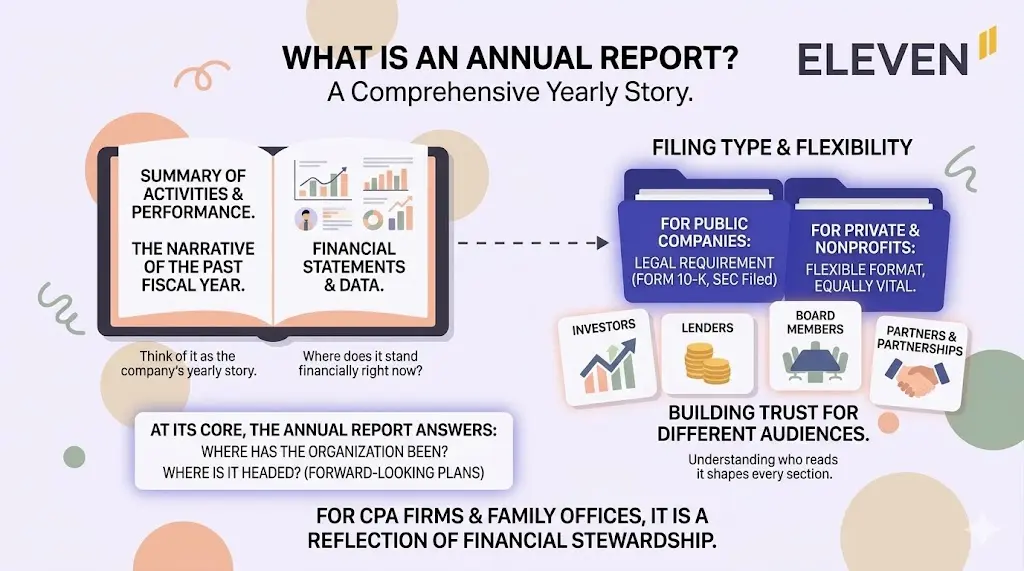

What Is an Annual Report?

An annual report is a comprehensive document that summarizes a company's activities, financial performance, and strategic direction over the past fiscal year. Think of it as the company's yearly story, told through numbers, narratives, and forward-looking plans.

For public companies, annual reports are a legal requirement filed with the Securities and Exchange Commission (SEC), most commonly as a Form 10-K. For private companies, family offices, and nonprofits, the format is more flexible but no less important.

These reports serve as a trust-building tool for shareholders, partners, lenders, tax authorities, and auditors.

At its core, a well-crafted annual report answers three questions: Where has the organization been over the past year? Where does it stand financially right now? Where is it headed?

The audience shapes everything. A family office annual report reads differently than a manufacturing company's 10-K, even if they cover the same core components.

Understanding who will read the report and what decisions they need to make from it should guide every section you write. Investors want to assess risk and return.

Lenders want to evaluate solvency and cash flow. Board members want accountability and strategic clarity. Writing one document that serves all of them requires deliberate structure and disciplined language.

For CPA firms and family offices, annual reports aren't just paperwork. They're a reflection of the financial stewardship you provide. Getting them right matters.

What to Include in an Annual Report

The structure of an annual report varies by entity type and audience, but the following components form the backbone of any solid report.

Opening Letter from Leadership

This is your chance to set the tone. A letter from the CEO, managing partner, or principal gives context to the numbers, acknowledging challenges, celebrating wins, and laying out priorities for the year ahead.

Keep it honest, specific, and forward-facing. Stakeholders read this first, and it frames everything that follows.

Avoid vague language and corporate boilerplate here. If revenue declined, say why. If a key client was lost or a market shifted, address it. Stakeholders who sense spin will distrust the rest of the report. A candid letter builds more confidence than a polished one.

Business Overview

This section describes what the organization does, how it operates, and what makes it distinctive. For a family office, this might mean outlining the investment philosophy and asset classes managed.

For a CPA firm's client, it would include the core business model, key markets served, and major developments during the reporting period: new service lines, acquisitions, leadership changes, or significant contracts.

This section should also address the broader environment the organization operated in during the year. Macro conditions, regulatory shifts, and industry trends all provide context that makes the financial results more interpretable.

Financial Statements

This is the heart of any annual report. The financial statements provide a verifiable, structured view of fiscal health. At minimum, these should include:

Balance Sheet -- A snapshot of assets, liabilities, and equity at year-end.

Income Statement -- Revenue, expenses, and net income or loss for the year.

Cash Flow Statement -- Operating, investing, and financing activities that affected cash.

Notes to Financial Statements -- Disclosures that explain accounting policies, contingencies, and material events.

For entities subject to audit, these statements will also include the auditor's report, a critical credibility signal for investors and regulators alike.

The notes are often underestimated. They document the assumptions and judgments baked into the numbers, and for sophisticated readers, they're frequently the first place to look.

Inconsistencies between the notes and the statements themselves are a red flag auditors and analysts catch quickly.

Management Discussion and Analysis (MD&A)

Numbers tell you what happened. The MD&A tells you why.

This narrative section gives management the opportunity to explain financial results in plain language: what drove revenue growth or decline, how expenses shifted, what the liquidity position looks like, and what risks lie ahead.

A strong MD&A doesn't just restate the income statement in paragraph form. It provides genuine analysis: comparing results to prior periods, explaining variances, discussing working capital trends, and addressing anything that materially affected performance.

For CPA firms advising clients, crafting a clear and candid MD&A is one of the highest-value contributions to the reporting process. It's also where automated bookkeeping pays dividends -- when your underlying data is clean and up to date throughout the year, writing this section becomes an act of analysis rather than archaeology.

Risk Factors and Internal Controls

Stakeholders want transparency about what could go wrong, not just what went right.

This section identifies the key risks the organization faces and explains what controls are in place to manage them. Common categories include market and interest rate risk, credit risk, regulatory and compliance risk, operational vulnerabilities, key-person dependency, and concentration risk in revenue or assets.

For family offices, this section is particularly important. It demonstrates the rigor of the governance framework and gives family members and trustees confidence that the office is operating with appropriate oversight.

For CPA clients, it also provides a basis for management's assessment of internal controls, which may be required depending on the size and structure of the entity.

Governance and Leadership

Larger entities and those with investor or board oversight should include a section on governance structure.

This covers the composition of the board or advisory committee, key leadership roles and changes during the year, compensation policies for executives, related-party transactions, and any material legal or regulatory proceedings.

For family offices, this section often documents the family's investment policy statement, the decision-making framework for major capital allocations, and the roles of key advisors. Clarity here prevents disputes and ensures continuity when leadership transitions occur.

What priorities will guide the organization in the coming year? What investments, partnerships, or structural changes are planned? What metrics will define success?

This section should be specific enough to be useful. Saying "we will focus on growth" tells stakeholders nothing.

Saying "we will expand into two new markets, reduce operating costs by 10 percent, and complete the transition to a new accounting platform by Q2" gives them something concrete to hold leadership accountable for at next year's review.

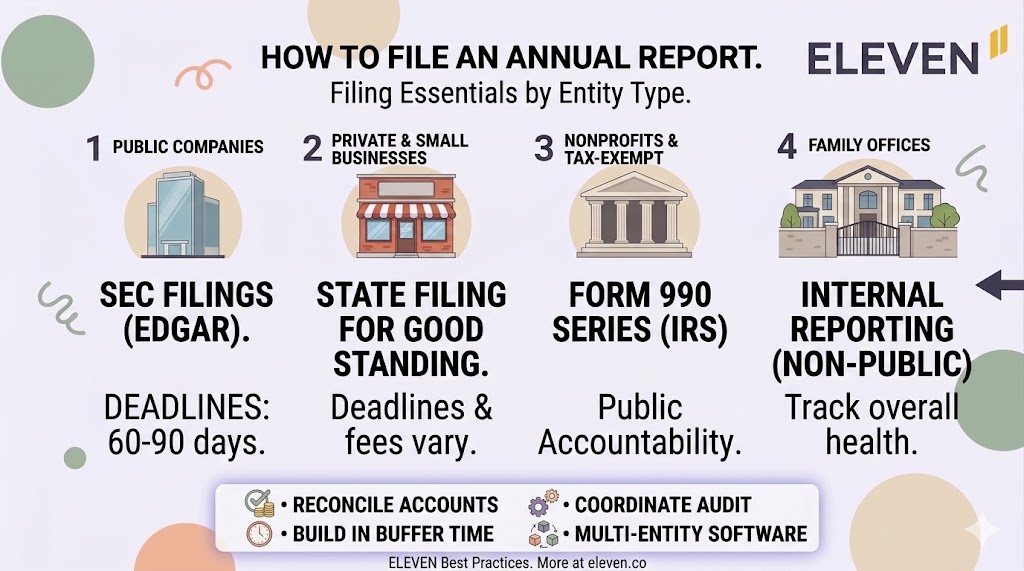

How to File an Annual Report

Filing requirements vary significantly depending on entity type and jurisdiction. Here's a breakdown of the most common scenarios.

Public Companies

Public companies are required to file annual reports with the SEC through the EDGAR system. The key filings to know:

Form 10-K -- The comprehensive annual report for domestic public companies. Due 60 to 90 days after fiscal year-end depending on company size.

Form 20-F -- The equivalent for foreign private issuers listed on US exchanges.

These filings must comply with GAAP (or IFRS for foreign issuers) and must be signed by the CEO and CFO, certifying the accuracy of the information under Sarbanes-Oxley.

Large accelerated filers have 60 days; accelerated filers have 75; non-accelerated filers have 90. Missing these deadlines triggers SEC scrutiny and can affect the company's ability to use certain registration statements.

Private Companies and Small Businesses

Private companies are not required to file annual reports with the SEC, but many states require an annual report filed with the Secretary of State to maintain good standing.

This is a simpler document, typically just a confirmation of registered agent, address, and officer information. Deadlines and fees vary by state, and failure to file can result in administrative dissolution of the entity.

Separately, private companies often prepare a full financial annual report for lenders, investors, or board members.

The format and depth of this report is typically dictated by loan covenants, shareholder agreements, or board charters. If your company has a credit facility, check the reporting requirements buried in your loan agreement: many require audited financials within 120 days of year-end, and missing that trigger is a technical default.

Nonprofits and Tax-Exempt Organizations

Tax-exempt organizations with gross receipts above $200,000 or total assets above $500,000 must file Form 990 with the IRS annually.

This is effectively their annual report. It's publicly available and covers finances, governance, executive compensation, and program activities.

Smaller organizations may file the 990-EZ or 990-N (e-Postcard). Missing this filing three years in a row results in automatic revocation of tax-exempt status, which is expensive and time-consuming to reverse.

Form 990 also requires narrative descriptions of program accomplishments, which function similarly to the business overview section of a corporate annual report. Boards and major donors frequently review these filings, so the quality of the narrative matters.

Family Offices

Family offices typically don't file public annual reports, but rigorous internal reporting is essential.

A comprehensive annual report for a family office consolidates investment performance across asset classes, documents entity-level financials for any operating businesses, tracks distributions and capital calls, and reviews the overall health of the family's financial plan.

The complexity here is often significant.

A single family office might encompass a dozen LLCs, trusts, and holding companies across multiple jurisdictions, with assets ranging from public equities to real estate to private equity positions.

This is exactly the kind of structure that multi-entity accounting software is built for -- consolidating all of that into a coherent annual picture requires both disciplined bookkeeping throughout the year and reporting infrastructure capable of rolling it up accurately.

Many family offices produce these reports for family members and their advisors, formatted with the same professionalism as an institutional report. Doing so reinforces governance, builds trust across generations, and makes audits and tax preparation materially easier.

Filing Best Practices for CPA Firms

Know your deadlines and build in buffer time. Late filings carry penalties and damage credibility with regulators, lenders, and clients alike.

Reconcile all accounts before drafting financial statements. Errors caught post-filing are far more costly than errors caught during review.

Coordinate early with auditors. Audit timelines affect filing timelines. Don't let one slip push the other past a regulatory deadline.

Standardize your chart of accounts and reporting structure across clients where possible. Consistency makes year-over-year comparisons meaningful and reduces the time it takes to prepare each successive report. This is one of the core arguments for multi-company accounting software over managing each client in a siloed system.

Document your review process. For SEC filers, SOX requires evidence of internal controls review. For private clients, documented review procedures protect both the firm and the client in the event of disputes.

Use software built for the complexity of multi-entity reporting, especially when managing multiple clients or a family office with layered entities across jurisdictions.

Make Annual Reporting Less of a Headache

Annual reports are only as good as the financial data behind them.

If your data is scattered across spreadsheets, legacy systems, or disconnected tools, every reporting cycle becomes a fire drill: hunting down numbers, reconciling discrepancies, and reformatting data that should already be clean.

Eleven is a cloud accounting platform built specifically for CPA firms and family offices. It consolidates multi-entity financials into a single, clean ledger, standardizes reporting across clients and entities, and gives you the kind of real-time visibility that makes annual reporting a process rather than a scramble.

See how it works with a free trial at runeleven.com/test-drive. No commitment, no sales pitch, just a faster and cleaner way to manage the financials that power your annual reports.

Noel Bouwmeester is an SEO content strategist and B2B SaaS writer focused on organic growth, search visibility, and AI-era content discovery. He has contributed to SEO and content marketing initiatives for companies including lempire and lemlist, helping support large-scale organic traffic growth through search-focused content strategies. At Eleven, he contributes educational SEO content focused on accounting technology, automation, and AI-driven business workflows.

.avif)