What Are Accounts (GL)? Definition, Example & How It Works

Learn what a general ledger (GL) is, how it works, and why it’s essential for accurate financial reporting. Discover how software like Eleven automates general ledger management and reconciliation.

What are Accounts (General Ledger)?

In accounting, a general ledger (GL) is the central record-keeping system for a company’s financial data. It contains an overview of all the accounts a company has, so you can track every financial transaction that has taken place over a period of time.

Think of it as the master book that summarizes all financial activity in the business.

The general ledger has a specific structure, made up of multiple accounts such as cash, accounts receivable, accounts payable, sales, expenses, equity, and more, with each account showing all debits and credits related to it.

Its purpose is to help businesses track financial activity, monitor account balances, and prepare financial statements like balance sheets and income statements, serving as the backbone of a company's accounting system.

It is important because it provides a complete, organized record of all transactions, ensuring accuracy through a double-entry accounting system where every debit has a corresponding credit.

It is essential for audits, financial reporting, and tracking a company's financial health.

What is general ledger reconciliation?

General ledger reconciliation is the process of verifying that the balances in a company’s GL accounts match external records or supporting documentation.

It ensures that the figures recorded in the accounting system are accurate, complete, and up-to-date.

For example, the balance in the cash account in the GL is compared to the company’s bank statement, while accounts receivable balances are checked against customer invoices.

Any differences between the ledger and external records are investigated to find the cause, which could be missing transactions, timing differences, or simple data-entry errors.

Once discrepancies are identified, adjustments are made in the general ledger to correct the balances. This might include recording a bank fee that wasn’t previously entered or accounting for deposits in transit.

The goal is to make sure the ledger reflects the true financial position of the business.

GL reconciliation is essential for maintaining the integrity of financial records. Accurate reconciliations ensure that financial statements, such as the balance sheet and income statement, are reliable for audits, and regulatory compliance, and for managers to make well-informed decisions.

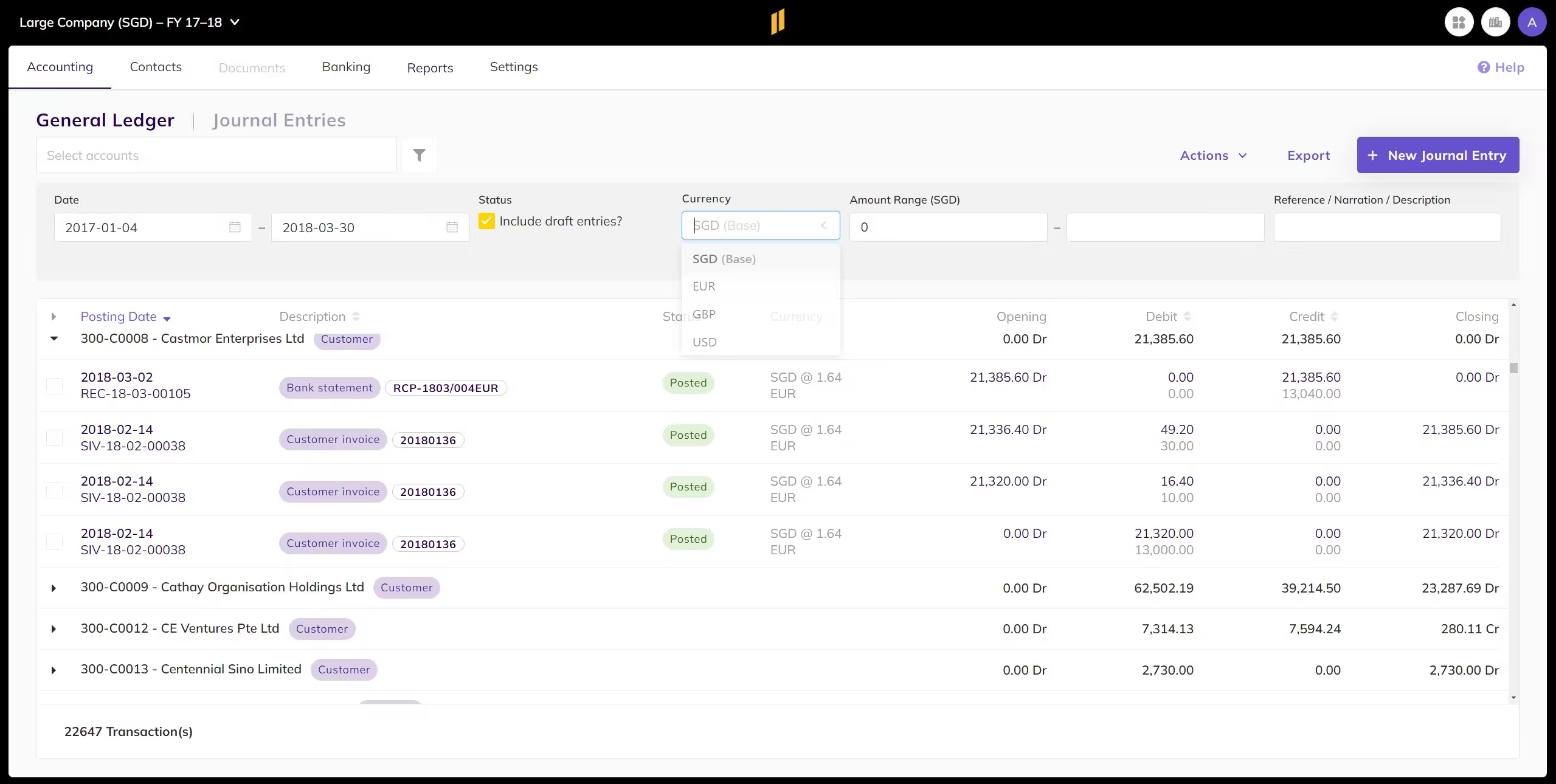

What does a general ledger look like?

Here’s what Eleven’s General Ledger looks like:

What does a general ledger tell you?

A GL provides the complete financial story of a business by showing the balances and activity of every account over time.

It allows you to see how much money is in each account, whether that is cash on hand, bank balances, money owed to the business through accounts receivable, money the business owes in accounts payable, inventory, or owner’s equity.

The general ledger also records every debit and credit affecting each account, making it possible to trace individual transactions, from sales and purchases, to expenses and loan payments.

By reviewing income and expense accounts, the GL reveals how much revenue the business has earned and how much it has spent over a specific period, providing the information necessary to create an accurate income statement.

At the same time, the GL organizes asset, liability, and equity accounts, forming the foundation of the balance sheet, which shows what the business owns, what it owes, and the owners’ stake.

Because every debit in the GL must match a credit, the ledger can also highlight errors or discrepancies in the accounts, helping to ensure accuracy.

Beyond tracking past activity, the information in the GL supports decision-making, giving managers and accountants the insight needed for budgeting, investing, and controlling costs.

How does a general ledger work?

A GL collects information from every financial activity and sorts it into accounts that show how money flows in and out of a business.

Here’s how it works step by step:

1. Recording transactions in journals

Every financial transaction starts as a journal entry.This could be a sale, a purchase, a loan payment, or an expense. Each transaction is recorded with a debit and a credit to the appropriate accounts. This is part of the double-entry accounting system, which ensures that the books always balance, that is, every debit has a corresponding credit.

2. Posting to the general ledger

Once transactions are entered in the journal, they are posted to the general ledger.Each account in the GL has its own page or section, and every debit and credit affecting that account is listed chronologically. For example, a sale paid in cash would increase the cash account (debit) and increase revenue (credit).

3. Tracking balances

The general ledger keeps a running balance for each account, so you can see not only what transactions occurred but also the current balance of that account at any moment.This allows businesses to know exactly how much cash, inventory, or outstanding liabilities they have at any given time.

4. Summarizing for financial statements

At the end of a reporting period, accountants use the balances in the general ledger to prepare financial statements.Asset, liability, and equity accounts form the balance sheet, while revenue and expense accounts create the income statement. The GL ensures that all financial data is accurate and complete for reporting purposes.

5. Error detection and audit trail

Because each transaction is recorded twice (once as a debit, once as a credit), the general ledger helps detect errors.If the total debits and credits don’t match, it signals that a mistake was made. Additionally, the GL provides an audit trail, so every transaction can be traced back to its source.

General ledger with accounting software

The right software can make maintaining a general ledger far simpler, faster, and more accurate. Traditionally, managing a general ledger involves manually recording transactions, cross-checking accounts, and reconciling balances - a process that is time-consuming and prone to errors.

A tool like Eleven automates much of this work for you, while providing real-time insights.

You can automatically capture and categorize transactions from bank accounts, invoices, and payments, posting them directly into the relevant general ledger accounts.

This eliminates the need for manual journal entries and reduces the risk of errors, ensuring that your accounts are always up-to-date.

Accounting software also makes reconciliation easier. Eleven can compare your ledger balances against bank statements, supplier invoices, or other supporting documents automatically, flagging discrepancies and suggesting adjustments.

Additionally, Eleven provides real-time reporting and dashboards, so you can instantly see account balances, track cash flow, and monitor financial performance.

It also simplifies audit preparation, as all transactions are digitally recorded, categorized, and traceable, creating a complete audit trail.

Overall, a tool like Eleven reduces manual work, minimizes errors, and provides clarity, giving businesses confidence that their general ledger is accurate and their financial reporting is reliable.

Recommended reading: How to manage general ledger (GL) in Runeleven?