.avif)

What Is Cloud-Based Automation & Its Benefits for Your Firm

Boost your team efficiency, capacity, and productivity while reducing costs with cloud based automation. Find out how our cloud accounting software can help.

AI is reshaping accounting workflows fast. Here’s where it adds real value, and where human expertise still matters most.

From automated reporting to smarter forecasting, AI is changing how accounting gets done. This guide breaks down the tasks being replaced, the value being created, and why accountants remain essential in turning data into decisions.

In this article

No: AI will not replace accountants.

However, it will automate many repetitive tasks and significantly transform the role of accounting professionals. AI is already replacing manual work such as data entry, invoice processing, and reconciliation. But it cannot replace human judgment, strategic thinking, or client advisory.

AI and automation have been gaining space quickly and surely. And accounting is seeing its impact too.

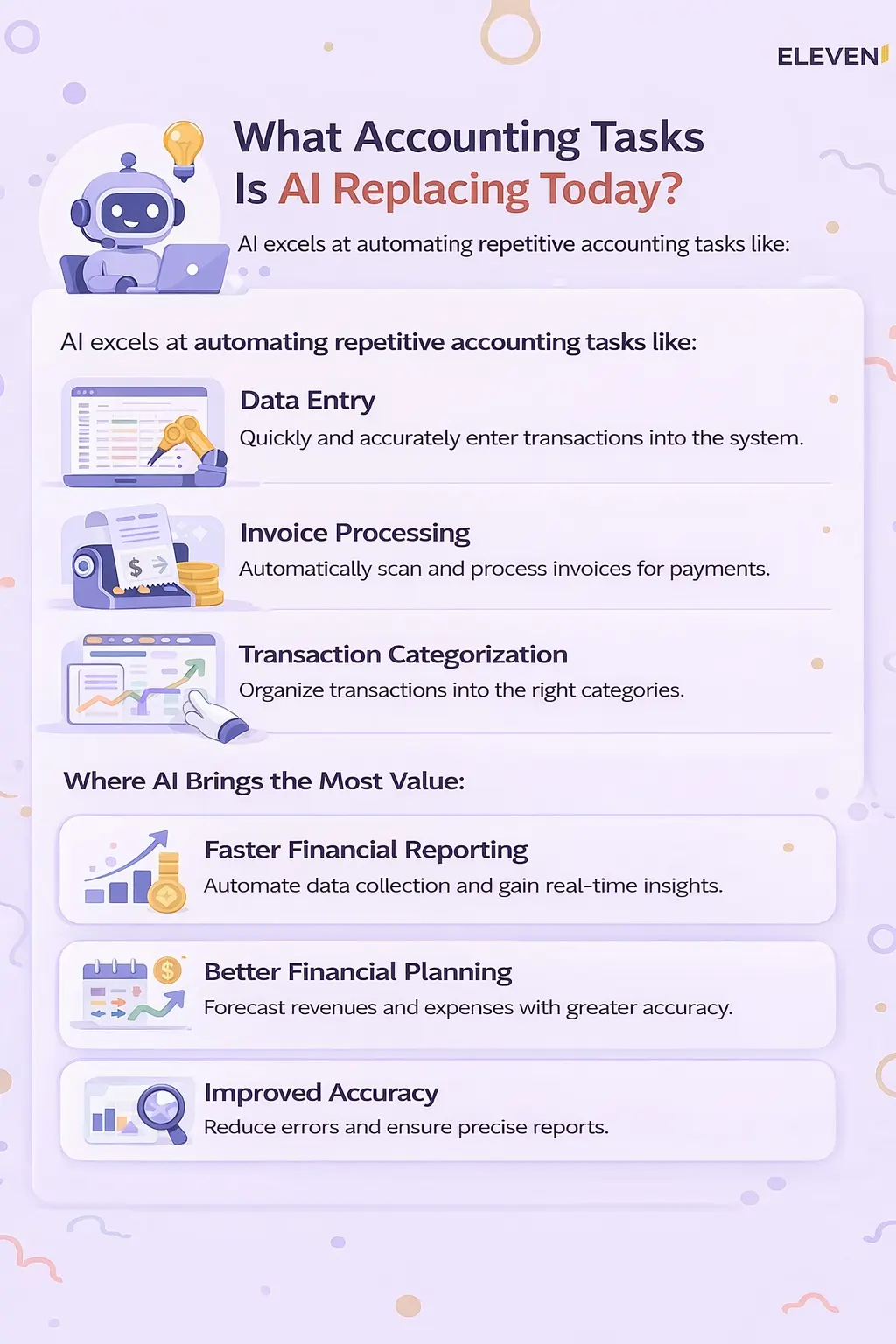

AI in accounting is now used to automate routine tasks such as bookkeeping, invoice processing, payroll, reconciliation, data entry, and financial reporting.

AI accounting software are financial management tools that use technologies including machine learning, natural language processing, and predictive analytics to guarantee efficiency and accuracy in accounting.

→ These tools use AI to identify patterns in financial data, automate decisions, and improve performance over time.

AI accounting tools can automatically categorize transactions, detect anomalies or fraud, predict cash flow, and generate real-time financial insights. This reduces manual work, improves accuracy, and helps accountants make better-informed decisions.

Forecasting also becomes more precise, which gives accountants a stronger role in strategic planning and advisory.

Automation has also reshaped audit procedures. AI tools can review large datasets quickly, identify unusual activity, and flag potential fraud far more efficiently than manual methods.

AI is good at doing repetitive tasks like data entry, sales automation, processing invoices, or even transaction categorization.

AI makes accounting software capable of handling repetitive tasks faster and more accurately. This reduces human error and frees up time for accounting professionals to focus on higher-value work.

Where AI brings the most value:

→ Faster financial reporting: AI tools can automate data collection, consolidation, and analysis throughout the reporting process. This makes reporting more efficient and gives firms access to real-time financial insights.

→ Better financial planning: AI planning and analysis tools can forecast revenues, expenses, and cash flow with a higher degree of accuracy. This allows firms to go beyond reporting and deliver more strategic value to their clients.

→ Improved accuracy: One of AI’s biggest strengths in accounting is its ability to reduce manual mistakes. Entering data by hand can create errors that affect final reports and lead to lost time, money, trust, and even clients.

That said, AI should not be treated as flawless. It helps improve data accuracy and keeps information more up to date, but its output still depends on the quality of the data entered in the first place.

This is why human expertise remains essential. AI can speed up processes and improve reporting quality, but accountants still need to review the data, interpret the results, and make sound strategic decisions based on context.

As we have mentioned earlier, accountants are now shifting toward a strategic approach.

In other words, instead of simply handing your clients reports of their finances and offering solicited advice, with the help of AI, you can offer a more complete service and offer strategic and proactive recommendations to help your clients make the most out of their business.

For example, instead of just reporting past expenses, you can use AI-driven forecasting tools to help clients plan budgets, manage cash flow, or identify opportunities for growth.

This is where (human) accountants become indispensable.

AI can generate data-rich reports and identify trends, but it lacks the professional judgment, ethical awareness, and industry context needed to turn that data into sound business strategies.

As an accountant, it’s now your role to interpret these AI-generated insights and advise clients or management on optimizing operations, mitigating risks, and ensuring compliance with evolving regulations.

Many routine accounting tasks, including data entry, bank reconciliations, invoice processing, and even initial audit procedures, can now be automated efficiently with AI.

For example, AI software can automatically match purchase orders to invoices or flag unusual transactions for further review. These capabilities significantly improve accuracy and reduce time spent on repetitive work.

However, while AI enhances efficiency, it does not eliminate the need for accountants.

Complex financial analysis, long-term planning, and nuanced decision-making still require human expertise. Critical thinking, ethical reasoning, and personalized client communication are skills that AI cannot replicate.

Don’t forget, AI lacks professional judgement and critical thinking skills that become necessary in working on more complex financial analysis and decision-making tasks.

Ultimately, to be a successful accountant in 2026, you should embrace technology as a powerful tool while focusing your efforts on high-value, strategic contributions.

Yet, with all the advantages AI brings into the profession, there are certain shortcomings of accounting concerning AI, there are still many limitations.

Some limitations include:

AI can process and analyze large volumes of data, but it lacks the human intuition, ethical reasoning, and professional skepticism that are essential in accounting.

For instance, detecting fraud or subtle financial irregularities often requires understanding intent, business context, or customer behavior.

Accounting decisions often depend on specific industry regulations, organizational goals, or market changes.

For example, interpreting a new tax regulation or adjusting reporting practices based on unique contractual obligations requires adaptive reasoning and contextual awareness.

Your role is to analyze numbers but also your client’s motivations, risks, and needs at that specific time.

AI is only as good as the data you provide.

Inaccurate, incomplete, or biased data can lead to incorrect results, flawed forecasts, or poor financial advice.

In accounting, even minor data entry errors can cascade into major inaccuracies in reports or compliance filings. AI cannot always detect when the data itself is flawed unless specifically trained with exception scenarios.

AI cannot create new financial models, rethink a business's revenue strategy, or assess qualitative factors like company culture in mergers.

Strategic planning, advisory services, and creative problem-solving is where you, as an accountant, shine and where you should focus on.

AI is a powerful complement to the accountant’s toolkit, but it is not a replacement.

Its limitations make human oversight and professional expertise more essential than ever in delivering reliable, ethical, and context-aware financial services.

At Eleven, we are dedicated to embracing the future of automated accounting by using the best technology in our accounting software, this makes your accounting process faster, more accurate, and more efficient.

With the use of AI, we strive to have workflows optimized, human error reduced, and real-time financial insights that deliver much better decision-making.

Our approach ensures that work relating to accounting professionals is only restricted to strategic, advisory, and interpretive roles that give more value to their organizations and clients.

Routine tasks in the domains of data entry, invoice processing, and generation of financial reports can be automated with Eleven's AI-based accounting software.

This allows accounting firms more time to work on more challenging financial analysis and strategy planning.

Eleven makes firms more efficient by automating these tasks and reducing a lot of human errors.

Some of Eleven’s features include scalable general ledger, multi-currency accounting, analytical accounting, automated bookkeeping, and much more.

Eleven takes compliance with financial regulations and ethical standards very seriously.

Our AI solutions, developed with rigorous security and privacy in mind, safeguard any form of financial information.

Further, it instils capabilities for fraud detection and prevention to ensure integrity in the financial reporting at firms.

Eleven's AI-driven analytic tools help accounting professionals arrive at the right decisions quickly by providing real-time insights into financial data.

They also keep firms one step ahead of the trends in the market, able to feel and adapt to changes in a very timely fashion.

This real-time capability is critical for firms that wish to provide timely advice or strategic guidance to their clients.

Eleven believes in constant improvement and innovation.

From time to time, we upgrade our software to keep pace with the advancement in AI and machine learning so that our clients can also avail of state-of-the-art tools. Eleven ensures that accounting businesses are ahead of their peers in an industry constantly changing.

AI will turn out to be incredibly useful as it automates routine tasks and gives individual accountants a boost in their capabilities.

Accountants will devote their time to higher-value tasks requiring critical thinking, professional judgment, and personalized service.

How can you avoid being replaced by AI?

Don’t stay behind! By rowing against the flow, you’re only going to hurt your accounting firm.

However, embracing a new and strategic role will guarantee that you remain relevant and essential to your clients.

After all, accounting is so much more.

If you’re ready to pair up with the best accounting software, try Eleven today

No, AI will not completely replace accountants. It can automate repetitive and rules-based tasks, but it cannot replicate human judgment, ethical reasoning, or strategic decision-making. Accountants are still essential when it comes to interpreting financial information, advising clients, and making context-based decisions.

The accounting roles most at risk are those focused on repetitive execution, such as data entry, bookkeeping, invoice processing, and basic reporting. These tasks are easier to automate because they rely on structured data and standardized workflows.

In the AI era, accountants need to develop skills that go beyond manual execution. Data analysis, financial strategy, advisory, critical thinking, and AI tool management are becoming increasingly important. Strong communication skills also matter more as accountants take on a more strategic role.

Yes, accounting is still a good career in 2026. The profession is evolving toward higher-value work rather than disappearing. As AI handles more repetitive tasks, accountants are becoming more involved in advisory, planning, compliance, and business consulting.

Related content

We are using cookies. Learn more.

%20(1).avif)